No, They're Not Killing the Digital Dollar. They're Merely Pausing It—Until 2030.

A Sunset Clause, FedNow, and the Road to a CBDC

So earlier this month, Treasury Secretary Scott Bessent stood in front of reporters and said that there would be “no central bank digital currency” under the Trump administration. (Of course, as you probably know, Bessent is one of Trump’s top people pushing regulated dollar stablecoins as the alternative.) New Fed Chair Kevin Warsh has said something similar.

Encouraging stuff.

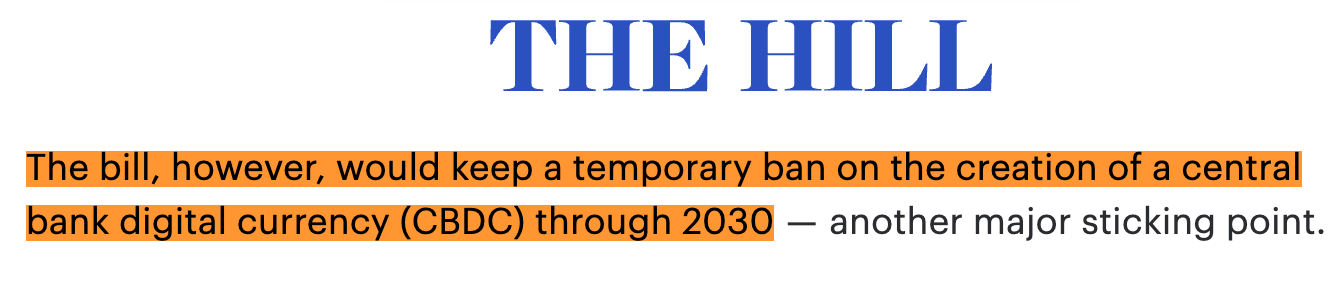

Especially since it comes on the heels of President Trump’s executive order, signed last year, directing federal agencies to halt any initiative to establish or promote a CBDC. Plus, Congress is currently working on a sprawling housing finance bill called the 21st Century ROAD to Housing Act, tucked inside which is a clause that would explicitly prohibit the Federal Reserve from launching a digital dollar.

You’d think, given all that, the question of a digital dollar was settled. Done. Closed file. Right?

See, there’s a small detail in that ROAD to Housing Act that’s escaped most of the coverage. The CBDC prohibition it contains comes with a sunset clause. It expires automatically on December 31, 2030. After that, unless Congress renews it, the ban just disappears.

Now, you’d be forgiven for asking the obvious question here. If the people writing this law actually wanted to kill the idea of a federal digital dollar, they’d have made the ban permanent. Why only until 2030?

Because they’re not killing it. They’re pausing it.

Granted, a handful of Republicans actually tried to make the ban permanent. Ted Cruz was probably the loudest of them. But they got rolled. Both parties' leadership wanted the sunset. That tells you everything you need to know.

And in the meantime, two things are happening.

First, as I wrote in a recent essay, there’s the GENIUS Act. Think of it as CBDC-level control without the baggage of the CBDC label — outsourcing the digital dollar to the likes of Tether and Circle (issuers of USDT and USDC, the two biggest dollar-pegged stablecoins). The government sets the rules. And the whole thing looks like just another tech product.

Second, in parallel, they’re quietly building the rails that’ll make a federal digital dollar work whenever they decide to switch it on. Regardless of what they end up calling it.

Let me show you what they’ve built so far.

The FedPal

You see, the Fed and big banks have been gearing up for the eventual rollout of a digital dollar for quite some time now.

As far back as 2017, a consortium including finance giants like Citigroup and JPMorgan initiated a real-time payments network operated by The Clearing House, known as the RTP Network.

This network processed a total of 173 million transactions worth about $76 billion during 2022.

The idea behind the RTP Network has always been to lay the technical groundwork and foster a culture of acceptance for a digital currency. The big banks made no secret of it.

But on July 20, 2023, the financial elites, led by the Fed, took it to a whole new level. Industry giants like JPMorgan, Citigroup and Wells Fargo lined up in support behind the project.

Thus, FedNow was born, the Fed’s own real-time payments service.

Officially, FedNow was meant to be like those instant payment apps you use, but for banks. It enables businesses and individuals to send and receive instant payments 24/7, 365 days a year. Sort of a FedPal, if you will.

Unofficially, though, FedNow is setting the stage for an all-digital dollar — or, as I like to call it, a Fedcoin.

By Design

FedNow is basically a test drive for CBDCs in banks.

That’s why the Fed is keen on rolling it out across the financial sector; they’ve made that much clear. Here are the words of Ken Montgomery, first vice president of the Federal Reserve Bank of Boston and FedNow program executive:

Availability of the service is just the beginning, and growing the network of participating financial institutions will be key to increasing the availability of instant payments for consumers and businesses across the country.

Expanding the Fed’s payments system to include more institutions, and ultimately reaching the public, is also a strategic move to drum up support for an eventual Fedcoin.

And the numbers since 2023 show exactly how aggressively they’re doing this.

As of today, more than 1,600 financial institutions are connected to FedNow — nearly 50% more than a year ago, and more than 45 times as many as when the service first went live. In 2025 alone, the system processed $853 billion in transactions, with an average payment value of just over $100,000 and total volume growing by 460% year over year.

If you open the official FedNow participants list (there's a downloadable Excel file on it, updated as of June 1, 2026), you’ll see some big names on it — BNY Mellon, Capital One, and the ones I’ve already mentioned, like Wells Fargo, JPMorgan, and Citibank.

This is already impressive, but there are plenty of reasons for others to follow. Think faster, more efficient fund transfers and improved liquidity management, just to name a few.

Banks have also been itching for a shot at the payments game, where fintechs like Venmo and Block’s Cash App have held sway. And FedNow could give them a competitive edge.

On top of that, the Fed recently proposed letting chains of correspondent banks use FedNow (today, a transfer can only involve two U.S. banks), and extending the service to handle the U.S. side of cross-border transactions.

Banks will inevitably see those “reasons” lining up with their business goals — and they’ll jump on the bandwagon.

Remember Them?

FedNow gives the Fed the ability to monitor every financial transaction made along with any data associated with that transaction.

That’s a scary proposition. Just think about it…

With this technology, the financial elites finally have the power, for the first time ever, to track every dollar you spend in real time. Not retrospectively, the way they could before. Not in aggregate. Live. Every wire, every transfer, as it happens.

Combine that with the GENIUS Act’s grip on stablecoin issuers (Tether, Circle, and whoever else gets a license), and the federal government now has visibility into a chunk of the dollar economy that was technically out of reach just five years ago. The Fed watches the bank rails. The Treasury watches the stablecoin rails. Between them, very little moves that isn’t observed.

And of course, if you can watch something, you can probably stop it too.

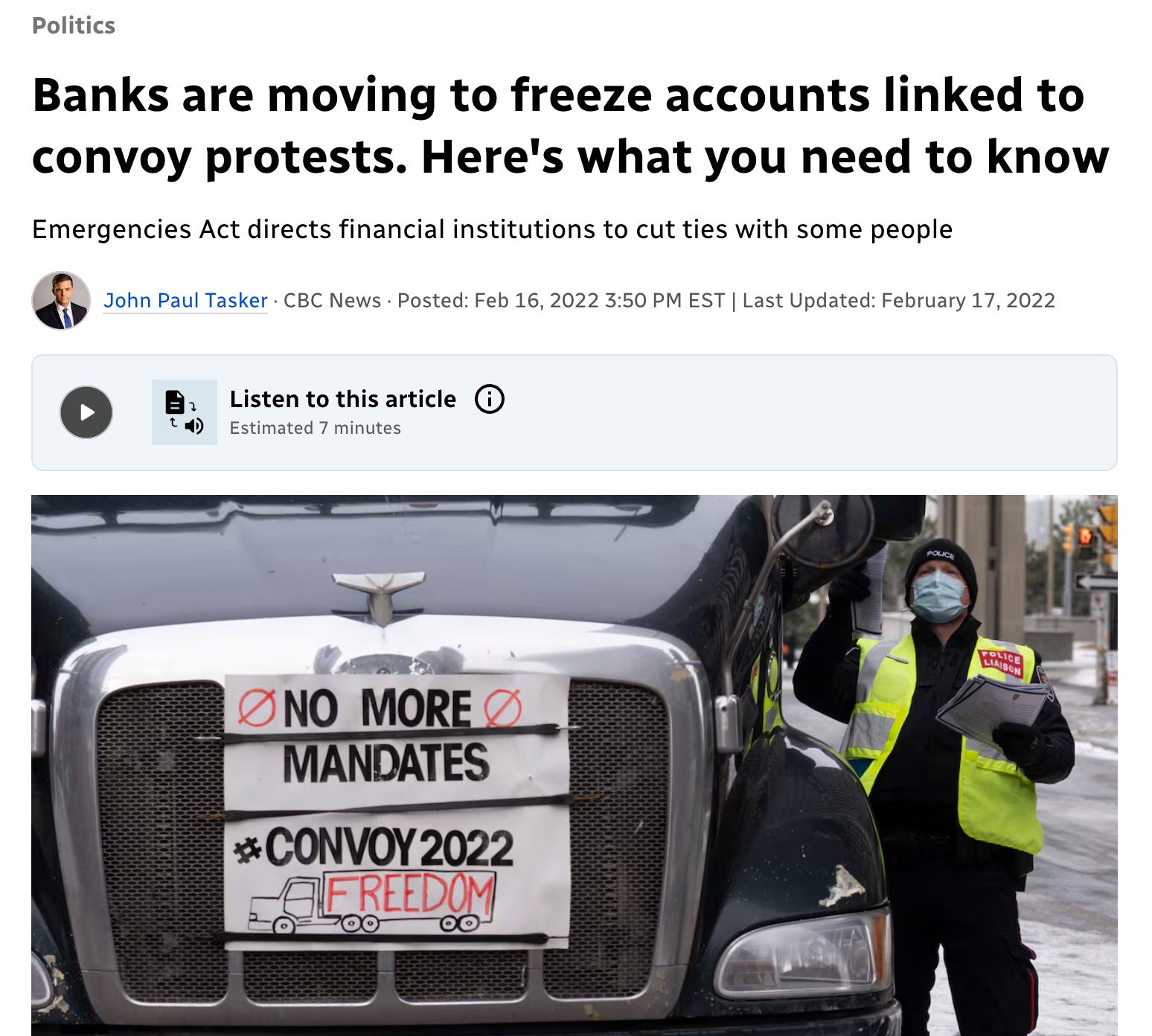

Before anyone tells you the kill-switch concern is paranoid, remember February 2022. Justin Trudeau invoked Canada’s Emergencies Act and ordered banks to freeze the accounts of trucker convoy donors. People who had committed no crime, who hadn’t been charged with anything, lost access to their money overnight.

The Fed will deny it. So will the government. They’ll talk about checks, balances, and regulation, but that’s the reality. And it’s getting us closer to the eventual rollout of Fedcoin, which, with FedNow spreading like wildfire, seems all but inevitable at this point.

None of the Trump administration’s recent CBDC announcements really change any of this. The 2030 sunset clause is the tell.

Regards,

Lau Vegys

P.S. There are things you can do to prepare for Fedcoin’s eventual arrival, regardless of what they end up calling it. First and foremost, hold hard assets — or what I call unprintable assets — like physical gold and silver. They've survived every monetary reset, currency debasement, and financial experiment governments have thrown at the public. And they can't be frozen with the click of a mouse. These days, that's a seriously underrated advantage.

They also keep putting a sunset into the NDAA. But that’s one they keep voting to continue.

It’s us against the US Government. As it always has been, is now, and ever will be.

Trump wouldn't do that , he loves us