China Is Cornering Silver—and My Second Recommendation

A forgotten export ban, a supply squeeze born in the Strait of Hormuz, and the best silver setup I see today.

Welcome to your second SNAFU Investing recommendation — as promised. Last week it was uranium; this week, silver. That pairing is deliberate: after uranium, silver is the sector I’m most bullish on in the world right now, and together the two of them anchor this portfolio.

The company — a silver miner I think the market has badly mispriced — and exactly how to buy it are waiting for you below. But first, the backstory, because with this one the why matters as much as the what.

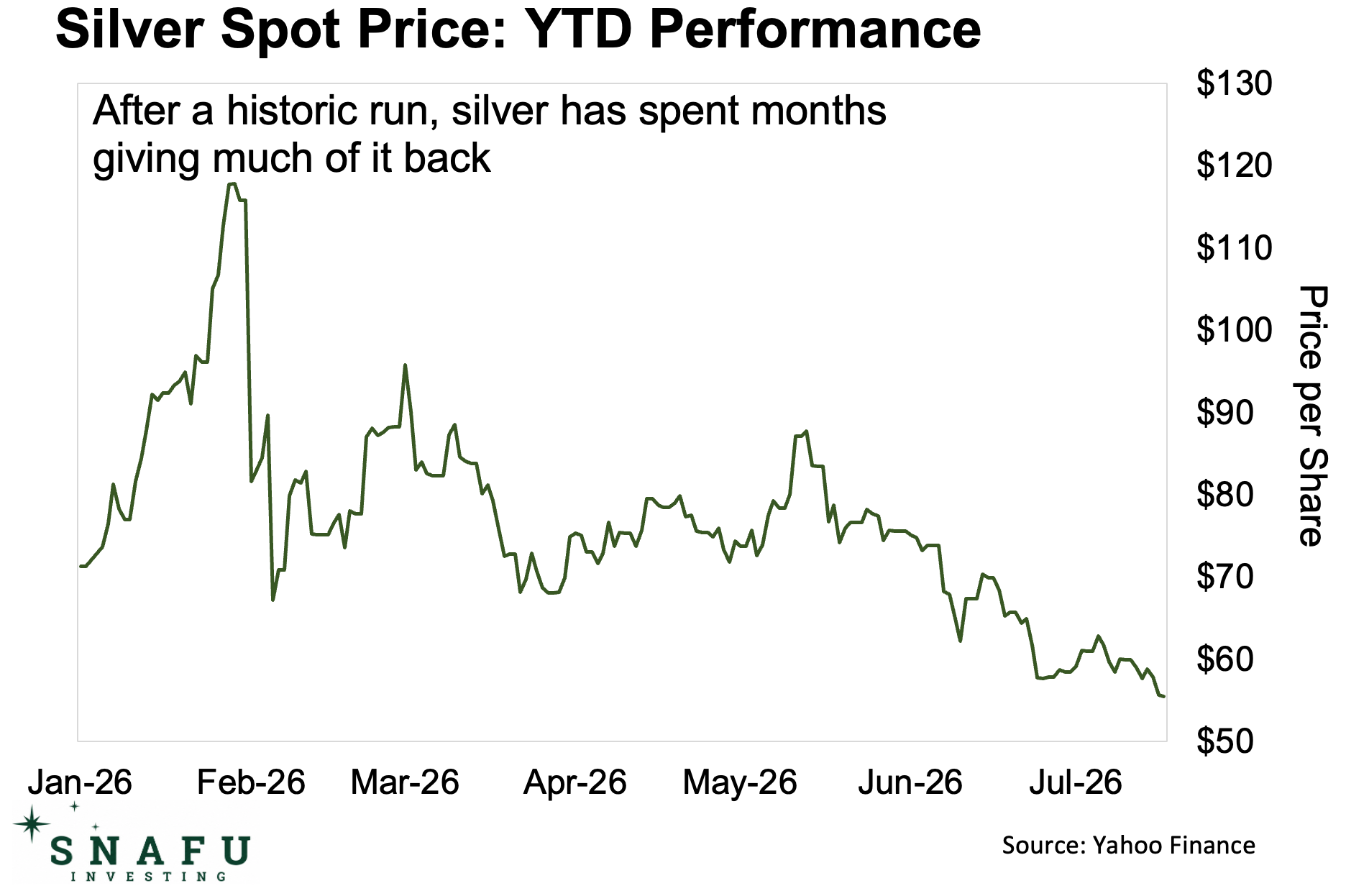

Now, as you probably know, at the start of this year silver did something it had never done before: it crossed $100 an ounce and went on to top $120. Since then, it’s been cut by more than half, trading around $56 as I write this.

Some people see a chart like that and run. I see an opportunity. Here’s why.

Yes, the silver price fell. But silver’s supply story didn’t — it got, well, even more bullish. In fact, 2026 is on track to be the sixth straight year the world consumes more silver than it produces.

In other words, the silver market isn't just in deficit. It's in a multi-year structural deficit.

And the reason that deficit persists comes down to supply. Industrial demand alone still consumes around 650 million ounces of silver a year — roughly 80% of everything the world’s mines produce — and mine supply simply can’t grow fast enough to catch up. The pipeline of large new primary silver mines is essentially empty; no major one is expected to come online before 2027. Even a standout like Aya’s Zgounder mine in Morocco produces only about 5 million ounces a year.

The Silver Squeeze

And it’s about to get worse — or better, depending on which side of the trade you’re on.

Now, if you read my article earlier this week, this next part will ring a bell. In it, I laid out how the fighting around the Strait of Hormuz choked off the world’s sulfur supply: roughly half of it ships through that single waterway, and when the Strait seized up, sulfur prices jumped about 70%. Then China — the largest exporter — halted most of its sulfuric acid shipments on May 1, tightening the screws further. (Sulfur is the main ingredient in sulfuric acid; right now there simply isn’t enough to go around.)

I told that story about uranium. But it's every bit as much a silver story — and here's why. Silver, you see, is barely mined on its own: roughly 70% of it comes out of the ground as a by-product of other metals, with copper alone accounting for about a quarter of global supply. And a good chunk of the world's copper is pulled from the ore using sulfuric acid.

Less acid, less copper, less silver.

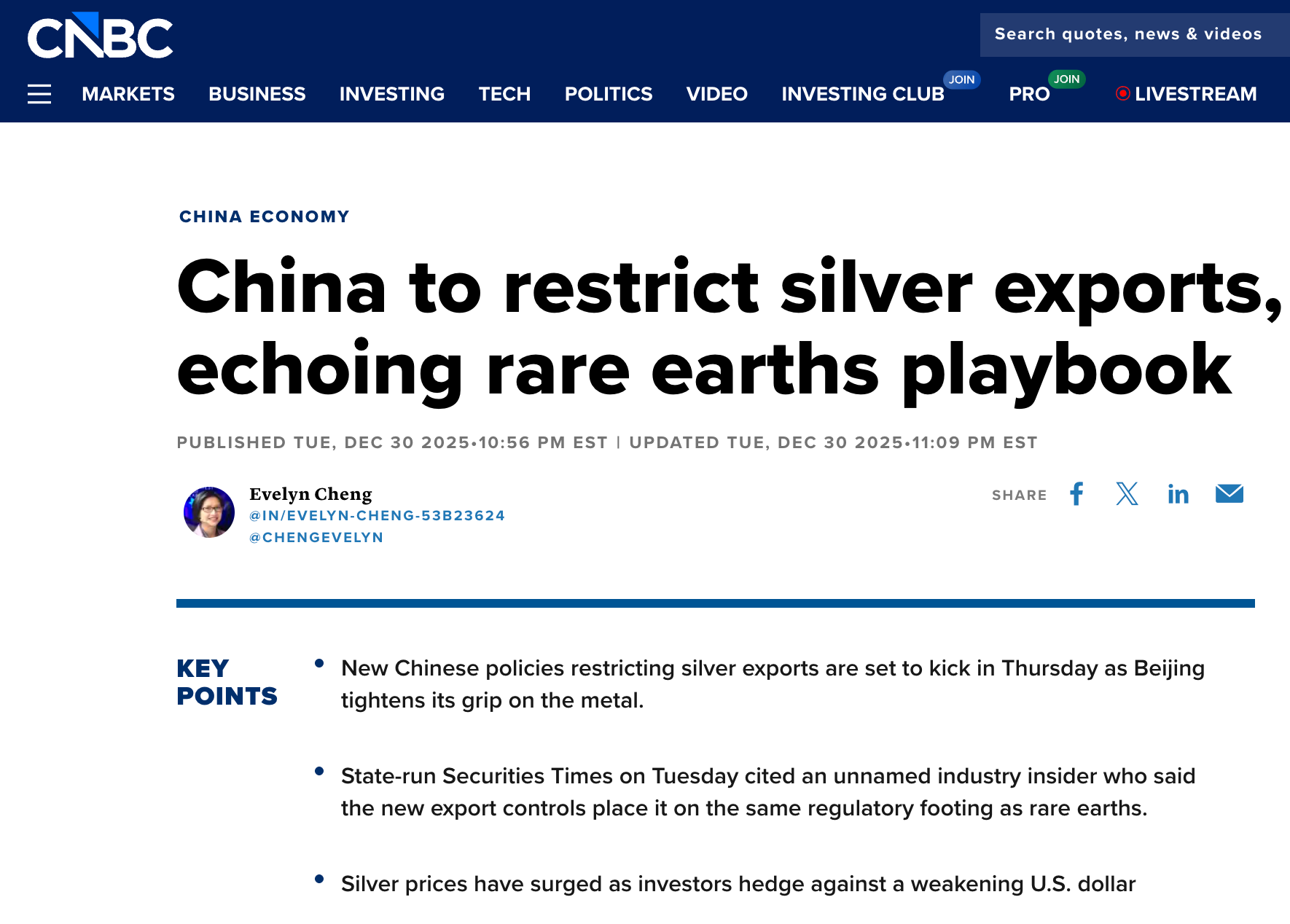

But here's the thing. That acid squeeze I just walked you through? As far as silver goes, it's only an indirect hit. And even China's role in it isn't its boldest move on the metal. For that, rewind to the first day of this year, to something most people have completely forgotten amid all the Hormuz headlines.

On January 1st, 2026, China reclassified silver under “dual-use export controls” — the rules reserved for materials that serve both civilian and military purposes.

In plain terms: exporting silver from China now requires government authorization. Only 44 companies have been approved to export silver during the 2026–2027 period, giving Beijing tight control over who can sell refined silver abroad.

If that sounds familiar, it should. It's the same playbook China used with rare earths. The difference is that, with rare earths, Beijing tightened the screws gradually — first permits, then more categories, then eventually even foreign-made products containing Chinese material.

With silver, it skipped all of that and went straight to comprehensive controls on day one.

And those controls remain firmly in place today.

Now, this matters a great deal because China controls 60–70% of the world's refined silver supply. So even when silver is mined in Mexico, Peru, or Australia, there's a good chance it still passes through Chinese infrastructure before it becomes usable metal. Beijing has effectively put itself in charge of whether that metal leaves—or stays.

A Different Animal Altogether

Now, you might be thinking: why does China care more about silver than rare earths? After all, rare earths are critical for all kinds of high-tech applications, right?

True. But rare earths, for all their strategic importance, are still relatively niche. They’re used in specific, high-value areas—mostly defense and advanced tech.

Silver is fundamentally different.

Solar panels. Electric vehicles. AI data centers. Military electronics. Satellites. Consumer devices. Medical equipment. 5G infrastructure.

I could go on. The point is, silver is everywhere.

And that isn’t a coincidence.

Silver is one of the best electrical conductors on Earth. What’s more, there’s no easy substitute for most applications. You can’t just swap in copper or aluminum and expect the same performance. Silver’s unique properties—its conductivity, its reflectivity, its resistance to corrosion—make it nearly irreplaceable in high-performance applications.

All of this makes silver’s demand what economists call inelastic. Think of it this way: if coffee doubled in price, some people would drink less—that’s elastic. But if insulin doubled in price, diabetics would still buy it—that’s inelastic. The demand continues regardless of price.

Now, the best way to play a silver bull market has always been through a leveraged silver miner. And below, I’ll give you the one that’s finally got me off the sidelines — a company that just cleared its biggest hurdle, yet is still trading as if nothing has changed. That gap won’t stay open for long — and I’ll show you why.

Remember: I put my own money behind every name I recommend here — but never ahead of you. I don’t buy for at least three trading days after a pick goes out, so you always get first crack at it.