Why I Never Go All-In on a Stock

How I manage risk in every speculative position, from tranches and stink bids to riding winners for free.

A few weeks ago, I wrote about the Monopoly set my father built by hand in the good ol' USSR (OK, maybe not that good). It was a personal piece about scarcity, resourcefulness, making something from nothing. It resonated with a lot of readers, but interestingly, what stuck with many of them wasn't the scarcity story. It was the part about my kids learning to take a calculated risk. When to buy, when to hold, when to walk away.

So today I figured I’d do something different and talk about how I think about risk with real money. Not Monopoly money. Specifically, how it applies to the kind of stocks I usually analyze and write about: resource stocks.

The approach to risk management I want to share with you today goes back to August 2024. I was editing Crisis Investing at the time, Doug Casey’s paid investment newsletter.

That month was anything but tranquil in the markets. Japan’s yen carry trade had blown up. The Dow dropped over 1,000 points in a single session. The S&P 500 fell 3.1%, wiping out US$2.1 trillion in market value. Oil plunged. Bitcoin cratered from US$60,000 to US$50,000 in hours. Even gold took a hit.

I was getting panicked messages from subscribers, and I realized something. Most of them didn’t have a system for any of this. They were either frozen, watching their portfolios bleed, or panicking and selling at the worst possible time. A few wanted to buy the dip but had no cash left because they’d gone all-in months earlier.

That experience made one thing clear: before we chase the next ten-bagger, we need to know how to protect ourselves when things go sideways and how to turn the panic into opportunity. So I put together a risk management playbook that month to help subscribers navigate the volatility of that year and beyond. That thinking is what I want to share with you today.

Fair warning: there's more arithmetic in this one than you're used to from me. Nothing sophisticated, I promise. But I hope you'll bear with me, because this might be one of the more useful things you read this year.

Position Sizing

Let’s start with the basics. Before you decide what to buy or when to buy it, you need to answer a more basic question: how much?

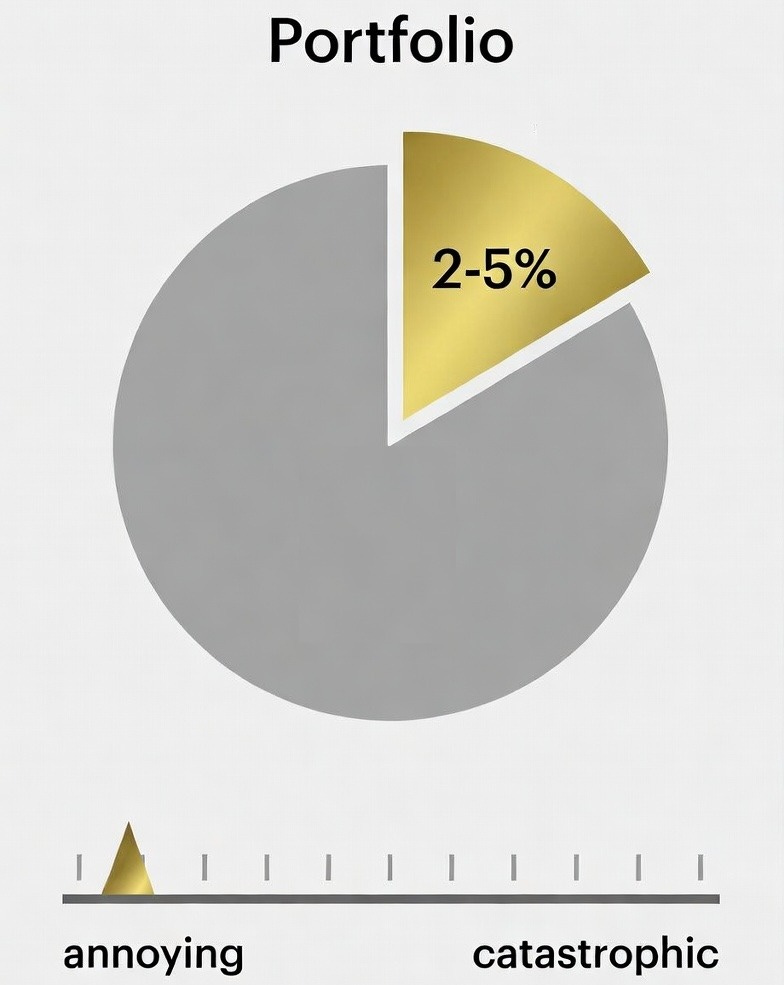

The rule I use is simple. No single speculative position should represent more than about 2–5% of your total portfolio. For the most speculative names, early-stage explorers and pre-production juniors, I cap it closer to 2%. For established producers with real revenue, maybe 5%.

The gut check is even simpler: if this stock goes to zero tomorrow, can you shrug it off and move on? If losing the entire position would change your behavior, delay your retirement, force you to sell other holdings, keep you up at night, the position is too large. Size it so that a total loss is annoying, not catastrophic.

This matters because the system I’m about to show you only works if you have the emotional headroom to be patient. If a single position is large enough to ruin your sleep, you’ll panic-sell at the worst possible time. And that’s exactly the opposite of what the next technique asks you to do.

Building Positions in Tranches

So you've sized your position. Now the question is how you get into it.

The biggest mistake I see people make (and I've seen it hundreds of times) is going all-in on a stock the day they decide they like it.

The problem isn’t the conviction. The problem is the timing. You might be right about the company, but the market doesn’t care about your timing. It’s going to do what it’s going to do. And if it drops 40% the week after you bought your full position, you’re sitting there with a massive unrealized loss and no cash to buy the dip you’d love to buy.

What solves this is not going all-in in the first place. Instead, you buy in tranches. Here’s what I mean:

First tranche (20%): When I decide to buy, I often start with just 20% of the position I ultimately want. This is my initial stake at the recommendation price. If the stock takes off immediately (rare, but it happens), at least I’ve got skin in the game. A win is still a win, even if it’s not as large as I’d hoped.

Second tranche (20%): Stocks dip. That’s what they do. When the stock pulls back, say 10–20% from my entry, I buy my second tranche at the lower price. Now I’m at 40% of my ideal position with a lower average cost than if I’d bought it all on day one.

The stink bid (60%): This is where the patience pays off. If the market suffers a major correction (and in the resource sector, it almost always does eventually), I place what’s called a stink bid. That’s an order set 40–50% or more below my entry price for the remaining 60% of my position. This is how you fill your position at a huge discount to the price you initially liked.

Yes, this strategy can be frustrating when the market is rising. You might find yourself with only 20% of your desired position while the stock takes off. But in my experience, sooner or later the resource market gives you an opportunity to buy lower. It’s just a matter of time. And until that opportunity comes, you’re rarely exposed to more than 40% of your ideal position unless you’re given a dirt-cheap chance to buy the rest.

Now, the 20/20/60 split you see above is what I use for the most speculative positions, pre-production juniors and early-stage explorers. But the split flexes based on the company's risk profile. For an established producer with cash flow and near-term catalysts, I might weight the earlier tranches more heavily, say 40/30/30. For a senior royalty company with decades of operating history, maybe 50/30/20. The principle is the same: don't go all in at once. But the more established the company, the less you need to hold back for a crash that may never come.

The math in a crash scenario

Say your ideal position is 10,000 shares of a gold stock trading at US$1.00. You buy your first 20%: 2,000 shares for US$2,000. The stock dips to US$0.90, and you buy your second tranche: another 2,000 shares for US$1,800. Now you're at 4,000 shares averaging US$0.95 (US$3,800 total).

Then the market crashes. A real crash, not a bad week. Your stock drops to US$0.50. If nothing is fundamentally wrong with the company, this is when you place your stink bid for the remaining 60%.

Your average cost basis is now US$0.68 per share (US$2,000 + US$1,800 + US$3,000 = US$6,800 for 10,000 shares).

If the stock eventually reaches US$10 (which happens in this sector more than people think), your 10,000 shares are worth US$100,000 on a total investment of US$6,800. That’s a 1,371% gain. And you built most of that position at fire-sale prices while everyone else was panicking.

The discipline required here is real. You have to be willing to sit on a fraction of your position while the stock climbs and feel like you missed out. You have to resist the urge to buy more when things are going well. And you have to have the courage to buy aggressively when everything looks like it’s falling apart.

That’s contrarian investing. It’s not comfortable. But it works.

Riding for Free

This is the other half of the system, and it’s just as important.

You’ve built a position using the tranche method, and the stock has doubled from your average cost. You’re sitting on a 100% gain. What do you do?

Most people do one of two things. They either sell everything and take the profit, which feels great until the stock triples from there. Or they hold everything and watch the gain evaporate when the stock pulls back, which feels terrible.

The better move: sell exactly enough shares to get your original investment back. Then let the rest ride.

The formula is simple:

If a stock has exactly doubled, the math is easy: you sell half. But it doesn’t have to be a clean double. If you’re up 90%, 105%, 120%, close enough. The formula works at any price. You sell just the number of shares needed to recoup your capital, and everything left over rides for free.

A worked example

You buy 10,000 shares at US$0.50 each. Total investment: US$5,000.

The stock runs to US$1.18. Not a clean double, but a strong gain of 136%. Do you wait for an exact double? No. You apply the formula:

5,000 ÷ 1.18 = 4,237 shares to sell

You sell 4,237 shares at US$1.18, getting US$4,999.66 back, essentially your entire US$5,000 investment. You still own 5,763 shares. They cost you nothing.

Now suppose the stock pulls back to US$0.70. Without the free ride, your original 10,000 shares would be worth US$7,000. That’s a 40% gain on paper, but you’d have given back most of your peak gain. Psychologically brutal.

With the free ride, you have your US$5,000 cash back plus 5,763 free shares worth US$4,034. Total value: US$9,034, an 81% return, with zero risk to your original capital.

And here’s the real power: if the stock eventually runs to US$5.00, those 5,763 free shares are worth US$28,815. You’ve made nearly US$34,000 on a US$5,000 investment, and your original capital was safely back in your pocket the whole time.

When Stop Losses Do Work

By now you might be wondering: what about stop losses? Aren’t those the standard risk management tool?

They can be. But it depends on the stock. Doug Casey famously warned that close stop losses on junior miners are just as likely to knock you out of a winning position as they are to save you from a losing one. And he’s right. But that doesn’t mean they’re useless. You just have to match the tool to the stock.

The distinction comes down to volatility. Every stock has a measure called beta, which tells you how much it moves relative to the broader market. A beta of 1 means it moves roughly in line with the S&P 500. A junior gold miner might have a beta of 2 or 3, meaning it swings two to three times as much as the index on any given day. A large-cap utility or a blue-chip dividend payer might sit at 0.5 or 0.6. It barely moves.

For low-beta stocks (large caps, index ETFs, stable dividend payers), a stop loss makes perfect sense. A 20–25% trailing stop on a stock that doesn’t normally swing more than 10% in a quarter is a reasonable safeguard. If it drops that much, something has probably changed fundamentally, and the stop gets you out before it gets worse.

Trailing stops are even better than fixed stops because they move with the stock. A trailing stop isn’t set against your purchase price. It’s set against the highest price the stock has reached since you bought it. Say you buy a stock at US$50 and set a 20% trailing stop. The stock climbs to US$75. Your stop is now at US$60 — 20% below the peak, not 20% below your entry. If it drops to US$60, you’re out with a 20% gain instead of a loss. The stop traveled up with the stock and locked in profit along the way.

But here’s where people go wrong. They treat stop losses as a one-size-fits-all solution. They slap a 25% trailing stop on a junior miner with a beta of 2.5 and wonder why they keep getting stopped out during perfectly normal trading weeks. A stock that routinely swings 30–40% in a quarter will trigger a 25% stop as a matter of course, not because something is wrong, but because that’s what volatile stocks do.

The point isn’t that one approach is always right and the other is always wrong. It’s that risk management is context-dependent. The picks matter, yes. But the risk management is what keeps you in the game long enough for the picks to pay off.

The worst thing you can do is use the wrong tool on the wrong stock, and that’s what most people do. Hopefully after reading this, you won’t be one of them.

Regards,

Lau Vegys

VISION BAD PARDON CAPS

DEAR LAU, EXCELLENT AS ALWAYS. YES, MONOPOLY TAKES ME BACK TO MY FIRST EXPERIENCE WITH THAT GAME MORE THAN SEVENTY FIVE YEARS AGO. REALLY FUN!

EXCELLENT INFORMATION ON “INVESTING”. I BREAK THAT DOWN INTO FOUR COMPONENTS—-LONG TERM INVESTING, SPECULATION, TRADING AND GAMBLING. ONE DAY, I HOPE TO WRITE AN ESSAY GIVING MY TAKE ON THOSE TOPPICS. BUT FOR NOW, JUST LET ME STRONGLY RECOMMEND AGAINST GAMBLING.

SINCERELY,

LIA\M OF LIAM’S LADDER

TYPE BY HIS ASSISTANT, LEJO

Hi Lau, good advice. What about Gold? does your logic about not going all in also apply to AU?