The Fed Is Quietly Abandoning Its 2% Inflation Target

For weeks the press cast Kevin Warsh as a hawk who'd finally get serious about inflation. And of course, he's anything but.

Earlier this week, on Wednesday, the Federal Reserve wrapped up the first meeting of the Kevin Warsh era and did exactly what everyone knew it would: nothing. Rates stayed at 3.75%. The market had the odds of any change above 95%, so the decision itself was a non-event.

But for anyone who stuck around, the press conference was the part worth watching. About halfway through, Warsh said something that should have been the headline.

When asked whether he planned to revisit the Fed’s 2% inflation target, Warsh said he tends to “focus on the left of the decimal point.” In plain English: as long as inflation starts with a 2, he isn’t going to fuss over what comes after it. 2.0%, 2.9% — same ballpark, as far as he’s concerned.

Now, personally, hearing that, I couldn’t help but chuckle. Because for weeks the financial press had been busy casting Warsh as a hawk, the tough new sheriff who’d finally get serious about inflation.

A hawk is supposed to sweat every last tenth of a percent. And here he was, in his first week, waving off the gap between 2.0% and 2.9% as a rounding error.

Note: It helps to know what that “2%” even points to. The Fed doesn’t target the CPI most of us see in the headlines. It targets a different gauge, the PCE price index, its own preferred yardstick, and, as luck would have it, the one that almost always reads cooler than CPI. Why cooler? Because PCE assumes that when something gets pricey, you’ll trade down to a cheaper substitute, and it folds in costs paid on your behalf, like employer health care. In other words, of all the official inflation numbers, the Fed is looking at the gentlest reading on the menu.

Then came the part I enjoyed most (and the part I’d seen coming the moment that left-of-the-decimal line left his mouth). Warsh announced a task force whose job is to “improve” the way inflation is measured. The current methods, he said, lean on “old-fashioned survey methods” that look “very little like the U.S. economy in 2026.” And when a reporter asked how, exactly, he’d improve them, Warsh allowed that he had “a phone call or two to make” before he could say.

You’d have to be brain-dead not to see what’s going on here — though, given some of the coverage of “hawkish” Warsh, apparently plenty are. The Fed can’t get inflation down to its target, so the new chairman’s headline idea is to go change the thermometer.

We’ve Been Here Before

And as I sat there watching, I couldn’t shake the feeling I’d seen this movie before. I had.

Back in October, Jerome Powell stood at a conference in Philadelphia and said this:

Normalizing the size of our balance sheet does not mean going back to the balance sheet we had before the pandemic.

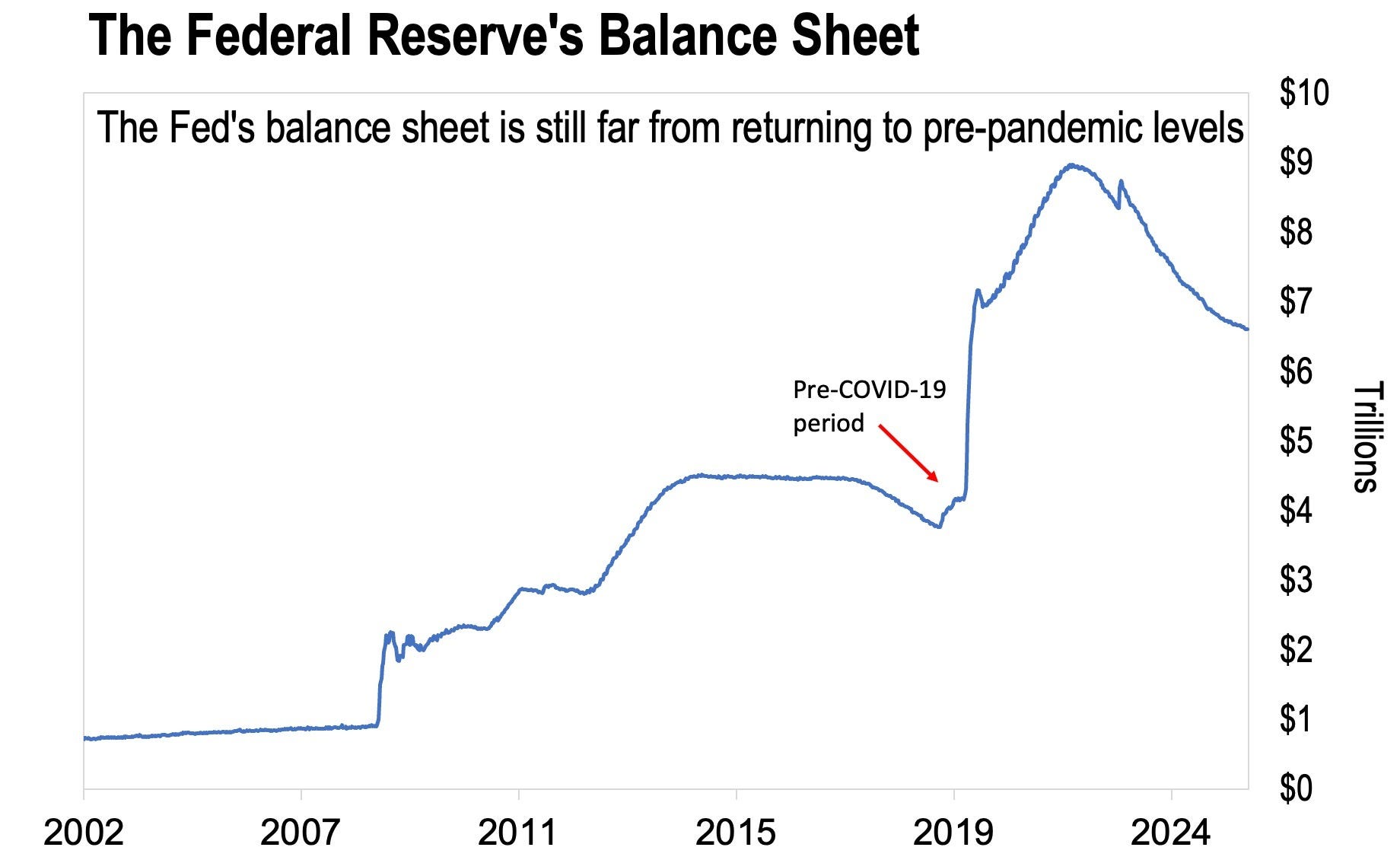

Ah, the balance sheet. The pile of bonds the Fed holds, every one of them bought with money it printed. It’s the cleanest measure there is of how much the Fed has conjured out of nothing.

Before the pandemic, that pile stood at about $4 trillion. To “fight” COVID, the Fed printed until it reached $8.9 trillion. The story sold to the public was that the printing would be followed by the great unwind — the long march back to normal, aka quantitative tightening. So how did that go?

Well, by the time Powell stepped up to that podium in Philadelphia, three-plus years of “tightening” had brought the balance sheet down to roughly $6.6 trillion. Nowhere near the $4 trillion it started from.

This was no accident. The honest way to unwind all that money-printing would have been to make the banks hand the cash back in exchange for their bonds. That was never going to happen. The Fed and the big banks are perfectly content to let the money slosh around Wall Street, lifting asset prices to record highs while the rest of us deal with the inflation. The other route, selling the bonds outright, risked crashing the bond market. So they chose the slowest, softest path there is: letting bonds quietly mature without replacing them.

And even that proved too much. So Powell just went ahead and said it. We’re done pretending. The new “normal” is $6.6 trillion. Deal with it. (And that was before he started buying again: $40 billion a month in fresh Treasuries, every month since December.)

Which is exactly what the new Fed chair is doing right now, only with the inflation target instead of the balance sheet. And once you’ve seen it, you can’t unsee it. Powell quietly buried the idea that the balance sheet would ever come back down. Warsh is quietly burying the idea that inflation will ever return to anything resembling "normalcy."

The One Thing They Can’t Do

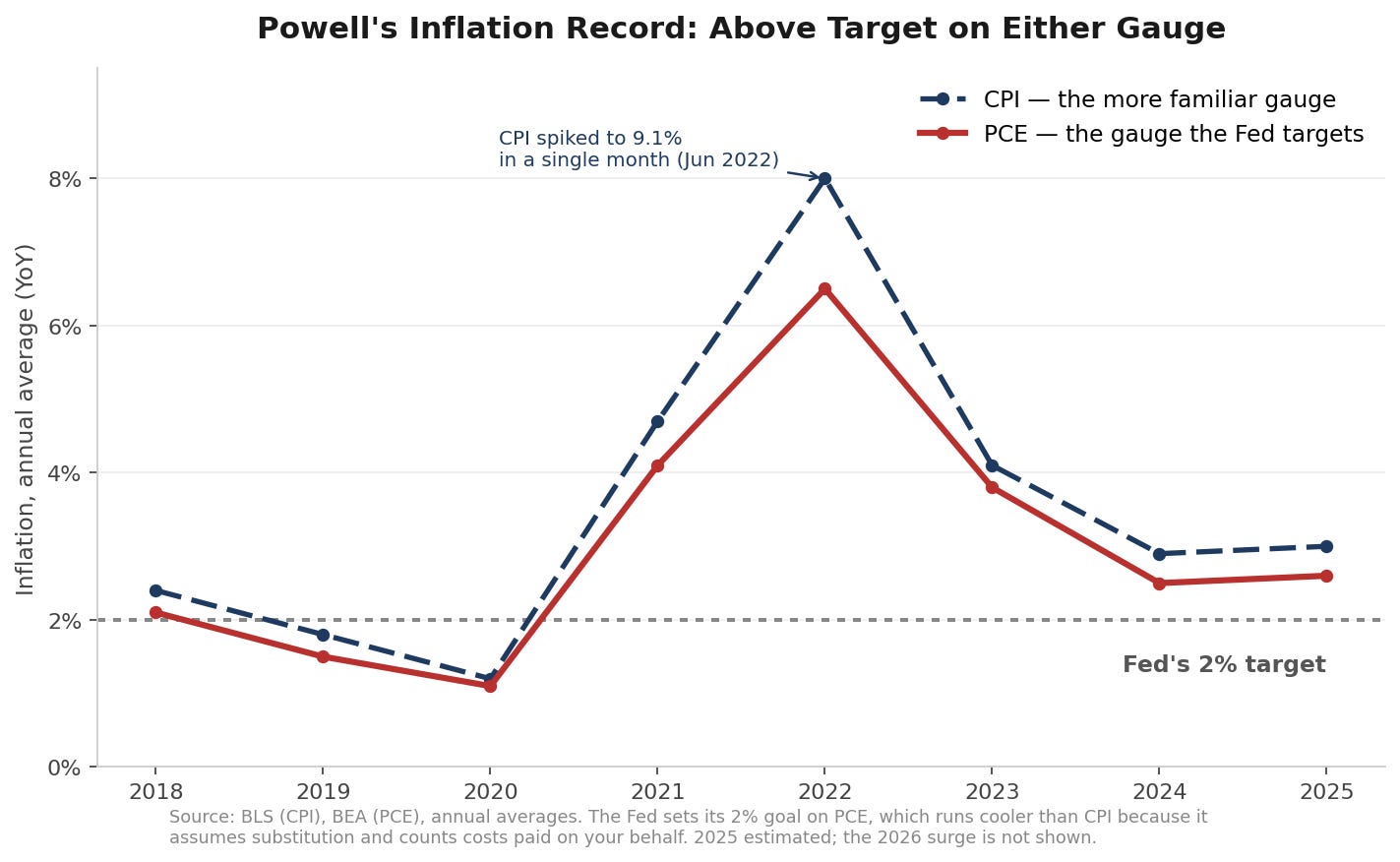

The 2% target was never going to survive contact with reality. Just look at Powell’s record.

Across his whole tenure, inflation ran well above the 2% he swore to protect — averaging around 3% on the Fed’s own preferred PCE gauge, and closer to 3.5% on CPI — with a 9.1% spike in 2022 that was the worst in four decades.

What did the Fed do about it? They cut rates. Three times in 2025 alone, while inflation was still running above target. This is the exact opposite of what you’d do if you were serious about fighting inflation.

Which is, of course, the one thing the Fed cannot do. Actually fighting inflation would mean the reverse of everything they’ve been doing: no more printing, pulling money back out of the system (real tightening), and holding interest rates high — on a national debt pushing $40 trillion that already carries an interest bill bigger than the entire military budget. Try it, and you blow up the federal budget and the bond market in the same motion.

So it was only a matter of time before they started moving the goalposts, which is exactly what we’re watching now. And whatever Warsh comes back with once that “task force” is up and running, don't kid yourself it ends there.

Remember, these are the same people who spent 2021 assuring us inflation was “transitory.”

At this point, it should be clear to everyone (even the most naive among us) that inflation isn’t a problem the Fed is solving. It’s a permanent condition the Fed creates and then pretends to manage, and the only part still under its control is the optics.

Regards,

Lau Vegys

P.S. There are things you can do to prepare for the coming dollar devaluation. First and foremost, hold hard assets — or what I call unprintable assets — like physical gold and silver. I know it sounds almost like a broken record by now, but it’s true: they’ve survived every monetary reset, currency debasement, and financial experiment governments have thrown at the public. And they can’t be frozen with the click of a mouse. These days, that’s a seriously underrated advantage.

They are already confiscating through inflation. Look at the unrealized capital gains tax in the Netherlands, the second property tax in NYC, and the billionaire tax proposal in CA. They will steal through legislation just like FDR (communist) did with his executive order for people to turn in their gold.

When the population realizes it can loot the Treasury by voting the game is over. The time to take action is yesterday.

I recall Jerome Powell attributed inflation to supply chain disruptions (which included factory shutdowns due to the pandemic), labor shortages....etc "Had people complied with immunization inflation would be behind us". Not verbatim but, close enough and who but the brain dead follows these disgusting people. What a racket.