Japan Just Raised Rates Again. Here's Why That's Your Problem Too.

For thirty years, Japan's cheap money quietly propped up Wall Street. That era is over.

What if I told you that something is breaking inside one of the world’s major economies — and it could have serious implications for your portfolio?

That economy is Japan.

I’ll get to all of it in due order, but let’s start with what’s most timely. Earlier today — literally just hours ago — the Bank of Japan raised interest rates to 1%. That’s the highest level since 1995. And it has made clear more is coming.

I realize you probably don’t spend much time thinking about Japan’s economy. Most people don’t. It’s on the other side of the world and doesn’t dominate headlines like the U.S. or China. By the end of this essay, I think you’ll see why it’s a very big deal.

So before we get into the meat of things, let’s establish one thing that will run through everything that follows: Japan isn’t just any country. It’s one of the biggest creditors on Earth — and, most important for our purposes, America’s single largest foreign creditor.

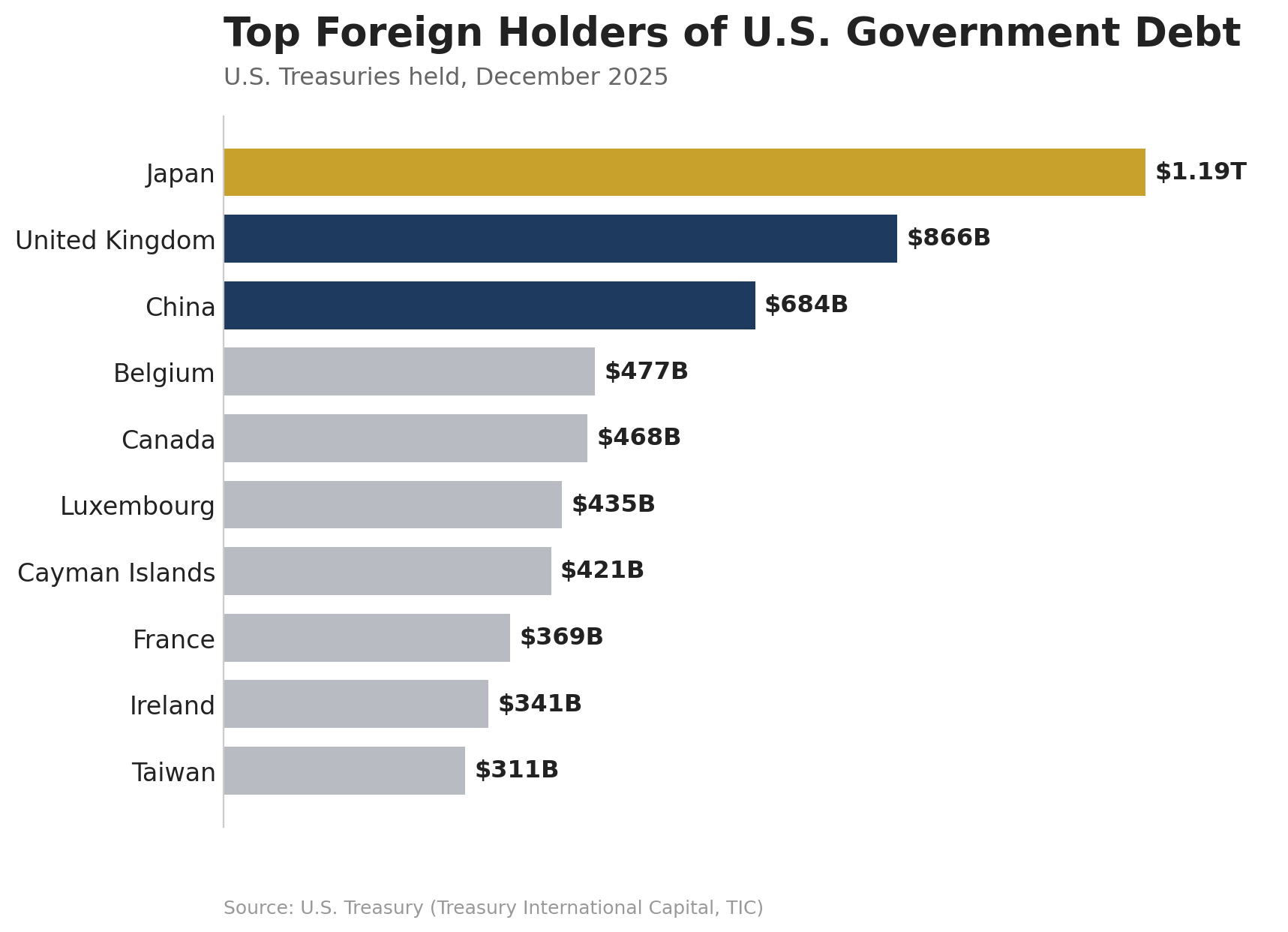

Japan holds more than $3 trillion in net foreign assets and is the largest foreign holder of U.S. Treasuries—nearly $1.2 trillion as of late 2025. Take a look at the graph below.

And it’s not just bonds. Japanese institutions have billions tied up in U.S. stocks, corporate debt, and real estate.

Which brings us to the question that matters: what happens if an economy as large and as deeply integrated into the global financial system as Japan suddenly needs to bring all that money home?

Japan’s Many Problems

To answer that question, you first need to understand the precarious position Japan finds itself in today. And it goes far beyond rising interest rates.

To start, Japan is facing a deepening population crisis. The nation’s population has declined for 16 consecutive years as fewer people marry and have children.

That’s not unusual — many developed countries are grappling with falling birth rates.

But not every developed country has one of the lowest fertility rates in the world. Japan recently hit a record low of 1.15, down from 1.2 the year before — the lowest since record-keeping began in 1947.

Keep in mind, you need a fertility rate of about 2.1 to maintain a stable population.

To make matters worse, Japan also happens to be the oldest country in the world. About 30% of its population is over the age of 65.

Combined, these factors mean that by 2050, Japan is projected to lose around 20 million people — about 16% of its current population. And by the end of the century, the country is expected to lose more than half its population. That’s like the entire state of Florida vanishing now, and most of the United States East Coast disappearing later.

This crisis affects far more than retirement homes and hospitals — it’s crushing the entire economy.

Fewer workers means less growth. More retirees means rising government spending. Every below-replacement-level country faces these problems, but when your fertility rate is plummeting toward 1 and you have the oldest population on Earth, you’re dealing with a whole new level of crisis.

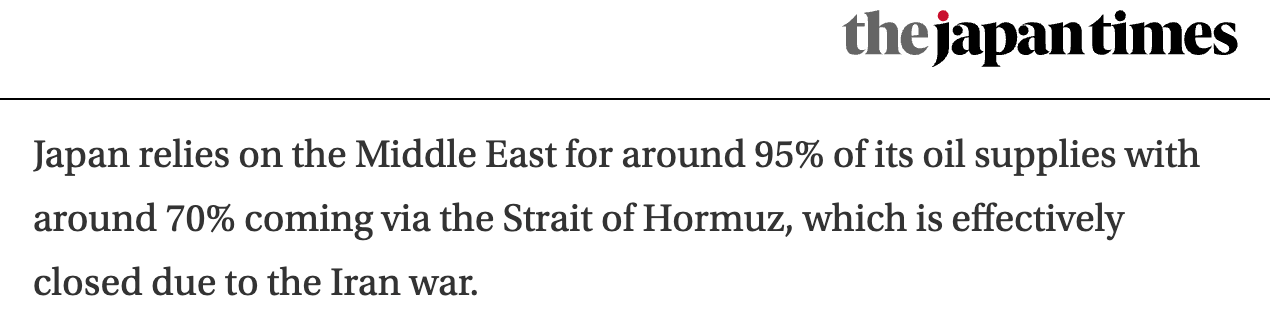

Second — and this one is ripped straight from today’s headlines — energy. Japan, you see, is an island nation with no meaningful domestic energy production. It imports nearly 90% of its total energy supply — not just oil, everything. And of its crude, 95% comes from the Middle East. And guess what: roughly 70% of that travels through the Strait of Hormuz.

You’d have to have been living under a rock to have missed what happened to that global chokepoint when the U.S. and Israel went to war with Iran, so I won’t belabor it. Suffice it to say that when Hormuz effectively closed, two-thirds of Japan’s oil supply was suddenly blocked, diverted, or severely disrupted.

Keep in mind, Japan has none of the cushions a country like the U.S. — or even China — can fall back on. No domestic production worth mentioning. No alternative pipeline routes. No preferential access through the strait. All it had was its reserves. And those started running low, fast.

The last time something like this hit Japan was 1973, the Arab oil embargo, and the country got absolutely pummeled — inflation surged past 20%. We don’t yet know whether this time will be as severe; the effects are still working through the system. But here’s what we do know: back then, Japan was young, growing, and relatively fiscally healthy. Today it’s none of those things.

Which brings us to Japan’s third problem: debt. And not just any debt — the heaviest load in the developed world.

That’s because the government’s long-running answer to everything I just described — the aging, the shrinking, the slow growth — has been to borrow. Heavily. As I write this, the country’s debt sits at over 260% of GDP.

Since the 1990s, Japan managed that burden with a familiar playbook: keep interest rates at zero and have the central bank print money to buy the government’s own debt.

The World's Biggest Free Lunch

Of course, one of the unintended consequences of keeping rates near zero for decades is that entire financial strategies get built around them. And in Japan’s case — being one of the largest economies on Earth, with the yen among the most-traded currencies anywhere — those strategies didn’t stay home. They were exported to the rest of the world. The biggest of them all, by far, was the yen carry trade — a machine for turning Japan’s cheap money into fuel for markets half a world away, including, in a big way, American ones.

Here’s how it works...

In a yen carry trade, large institutions borrow Japanese yen at rock-bottom interest rates. Then they convert that cheap money into dollars and plow it into higher-yielding assets abroad, especially in the U.S.

Imagine you’re a trader who borrows 10 million yen when the exchange rate is 100 yen to the dollar. That gives you $100,000 to play with. You dump this money into U.S. Treasury bonds yielding 4%. After a year, you’ve pocketed $4,000 in interest. And it gets even better — if the yen has weakened to 105 yen per dollar, you only need $95,238 to repay your loan. You’ve profited not just from the interest rate difference, but also from the currency move.

It’s essentially free money. At its peak, Bloomberg estimated yen carry trades reached hundreds of billions globally. Traders had been milking this cash cow for decades. Some people called it “the global money glitch.”

But there’s a (predictable) catch.

This strategy only works as long as Japanese interest rates stay low and the yen remains weak.

If either goes the wrong way, the trade breaks.

We got a preview of that back in August 2024, when the BoJ finally blinked — raising rates to 0.25%. Suddenly, the math flipped. Traders now needed more dollars to repay their yen-denominated loans than they had borrowed. That triggered a violent unwinding of positions — and a cascading sell-off across global assets that wiped out over $5 trillion in market value.

When the Bill Comes Due

Now, the Bank of Japan isn’t raising rates because it wants to. When you’re carrying this much debt, even tiny rate increases are brutally expensive.

It’s being forced to.

Bond investors are demanding higher yields. Japan’s auctions are failing. The BoJ, already holding 50% of the government bond market, is increasingly buying alone. Foreign and domestic investors are either fleeing or demanding much higher rates to offset inflation and currency risk.

So the BoJ is capitulating, and you can watch it happen in the numbers: 0.25% back in August 2024, 0.75% last December, and now 1%.

And here’s the thing.

Even if the immediate crisis in the Middle East eases, Japan's problems won't. The damage is already done. Japan’s oil supply is gutted, its trade deficit is blowing out, and the very inflation that started the BOJ down this road is running hotter still. That’s what carried them from 0.75% in December to today’s 1% — and it’s why they won’t be stopping there as the inflationary effects keep filtering through.

Thanks to Japan’s uniquely bad position — the problems I outlined earlier — there just aren’t any other options. The alternative would be even more trouble selling their debt, along with a yen free fall that would make imports ruinously expensive. And I do mean ruinously — Japan imports 60% of its food and, as already mentioned, nearly all of its fossil-fuel energy.

But rising rates in Japan don't just spell trouble for Japan. They spell trouble for you.

Remember, Japan holds nearly $1.2 trillion in U.S. Treasuries — more than any other country. As Japanese rates rise and the yen strengthens, parking money in America stops making sense. And so, instead of financing Uncle Sam's debt binge, that capital starts heading home.

Last year, Japan’s finance minister even floated the idea that their U.S. Treasury holdings could be “leverage” in trade talks. He later backtracked — but the message was clear: nothing is off the table in hard times.

That's the thing about a creditor this size: it doesn't need to do anything dramatic. Even the appearance of it stepping back would send a chill through global markets, undermine confidence in U.S. debt, weaken the dollar, and push borrowing costs higher across the board.

And it doesn't even have to sell a single U.S. Treasury for the damage to reach American markets.

Given how deeply Japanese capital is woven into the global financial system, even repatriation from other markets can send shockwaves across asset classes. It’s a domino effect. Capital flowing back to Japan from emerging markets tightens global liquidity — and that tightening eventually hits Wall Street just as surely as if Treasuries had been sold outright.

Now, I don’t expect this to look like August 2024 — one violent, single-day crash.

No. The pain from Japan's rising interest rates is more likely to unfold in slow motion. Funding costs rise. Leverage becomes unbearable. Positions get unwound, one by one, as the math stops working. And one day you look up and wonder why a portfolio full of perfectly good (mainstream) stocks has been quietly bleeding red for months.

Regards,

Lau Vegys

P.S. A quick note. I want to say thank you, sincerely, to everyone who has pledged their support over the past few weeks. I’m doing my best to reach out to each of you individually in private, but in case I missed anyone, thank you, again. Whether you’ve reached out publicly, privately, or just quietly clicked through to subscribe, I value it enormously.

Great writing. I love the way Lau explains things.

“One day you’ll look up and wonder why … “ Well, forewarned should leave us prepared to make the requiste changes before it’s too late and we’re surprised and hurt. Thanks for your good work and lucid explanations.