Iran Won? The Fed Moved the Goalposts. Macron Hosted the AI Cartel.

Last week, in the rearview.

Last week’s biggest story came out of the Middle East. After months of a useless war, the U.S. and Iran announced a tentative 14-point framework to end the fighting and reopen the Strait of Hormuz. Markets celebrated: Brent crude dropped to $83 a barrel, a three-month low; stocks rallied; the world exhaled.

Seems like a bit of an over-the-top reaction, if you ask me — given that the main route through Hormuz still has 80 unswept mines, with the southern route through Omani waters quietly doing all the actual moving. And honestly, I’m still struggling to figure out what the U.S. actually got out of this. What we do know is what Iran got: the U.S. naval blockade lifted, broad sanctions relief, and roughly $24 billion in previously frozen assets released. And more important than any of that, the lesson Iran has just etched into the playbook is brutally simple: they can shut Hormuz any time they want, and no one — not even the most powerful military on earth — can do much about it. So again, what exactly did the U.S. get out of all this?

Last week was also a busy one for the central bankers.

On Wednesday, Kevin Warsh wrapped up his first Federal Reserve meeting. The rate decision — a hold at 3.75% — was a non-event. But about halfway through the press conference, the new chair basically told you the Fed is giving up on its 2% inflation target. I broke down what’s actually going on in Saturday’s piece.

Across the Pacific, the Bank of Japan (BoJ) went the other way — on Tuesday they hiked their key rate by 25 basis points to 1%, the highest level since 1995.

Why does this matter so far beyond Tokyo? Because Japan is the world’s largest single foreign holder of U.S. Treasuries, and they’re being forced to hike because their own inflation refuses to quit. When Japanese rates climb, the math on parking trillions in American debt — instead of redeploying it at home — starts to fall apart fast. I wrote up the implications for U.S. investors in Tuesday’s piece.

Meanwhile in Europe, the European Central Bank (ECB) went the BoJ’s way — hiking rates 25 basis points and citing “inflation pressures” from the Iran war. This in the same week the eurozone’s first-quarter contraction was confirmed, the ECB revised its own inflation forecasts higher, and German industry kept bleeding jobs. In short, things aren’t looking good for the old continent. And as I wrote in Thursday’s piece, history says when Europe stumbles, America catches the chill too.

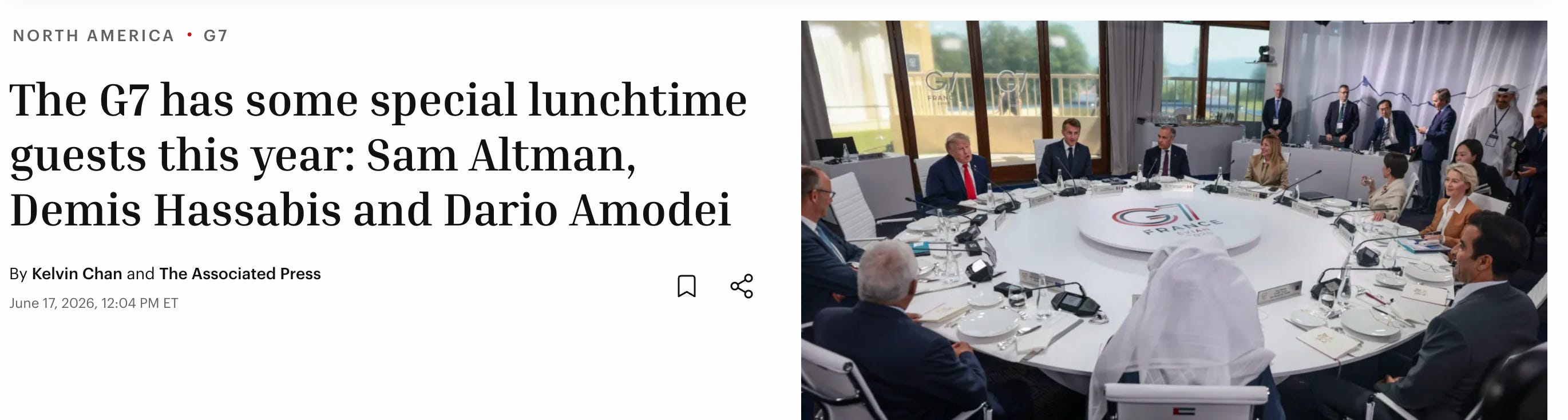

Last week also saw the annual G7 summit (the gathering of the world’s seven largest advanced economies), hosted by President Emmanuel Macron in Évian-les-Bains, the French spa town on the shores of Lake Geneva. The moment that caught my eye most was Macron inviting the CEOs of OpenAI, Anthropic, and Google DeepMind to a working lunch with heads of state. Sam Altman, Dario Amodei, and Demis Hassabis each got bilateral photo-ops with the French flag behind them, sitting in chairs usually reserved for presidents and prime ministers.

Curiously, this came just days after Trump banned foreign access to Anthropic's most powerful AI models. Even more curiously, those same three CEOs spent the summit asking for more regulation. The regulation, of course, helps the incumbents most. But that’s just one of many implications — I’ll probably sit down to write about it properly in the coming weeks. By the way, both OpenAI and Anthropic filed for IPOs last week, targeting fall debuts at roughly $1 trillion each. The next two index forced-buyer events are now on the calendar (following the SpaceX IPO on June 12, 2026).

And now for the latest pieces…

The Fed Is Quietly Abandoning Its 2% Inflation Target

Earlier this week, on Wednesday, the Federal Reserve wrapped up the first meeting of the Kevin Warsh era and did exactly what everyone knew it would: nothing. Rates stayed at 3.75%. The market had the odds of any change above 95%, so the decision itself was a non-event.

Europe's Recession Is Coming for America

When I’m in Europe, I usually split my time between Lithuania and Spain. We leave for Spain in a few weeks, so I’ve been trying to make the most of Vilnius before we go. It’s a quietly beautiful, underappreciated city, the capital of what was once one of the largest states in Europe, with the history to match. There’s plenty to see.

Japan Just Raised Rates Again. Here's Why That's Your Problem Too.

What if I told you that something is breaking inside one of the world’s major economies — and it could have serious implications for your portfolio?

From the Comments

One of the things I’ve come to appreciate most about writing here is the conversation that happens in the comments. The thinking there often sharpens my own and adds dimensions I’d never have thought to include. Last week was an especially rich one on that front. Note that each of the (seven) reader comments below links back to the piece or note it appeared on, so you can click through if you’re interested in the context.

Thanks again to everyone who left a comment last week. I read all of them, even the ones I don’t get a chance to reply to individually. Over the coming days, I’ll try to catch up on the questions and the longer threads.

See you in the comments this week.

Regards,

Lau Vegys

Perhaps the goal was to let China know that the U.S. now can control the oil flow of the world. Mission accomplished.