How I Found a Five-Bagger in Rare Earths

The trade from start to finish—and the two things I look for before putting money behind an idea.

I had a hell of a year in 2025. Both as a newsletter editor and as a guy who puts his money where his mouth is. Gold was up 60%. Silver surged 160%. And though many precious metals stocks trailed the metals themselves, the portfolio I was running at Doug Casey’s publication delivered in spades. Precious metals holdings averaged roughly +140%. Across all the recommendations I made in 2025, the average return was +53%. And along the way, I issued 11 separate alerts for subscribers to take their initial capital off the table and ride the rest for free.

But arguably the call I'm most proud of is the rare earths.

So today I want to walk you through that trade from start to finish. How I identified the opportunity, why I picked the company I did, and how it played out. Not because of the return (though it’s done very well, as you’ll see), but because I think it’s the clearest way to show you how I approach these investments. Every winning trade looks obvious after the fact. Hindsight makes the result look inevitable, when what actually matters is whether the process that produced it was repeatable (which in my case it is, because it follows a specific framework). So I think it’s a useful exercise, and I hope you’ll find it interesting.

Before I get into it, I wanted to thank everyone who read and especially those who reached out about my “what happened” essay. I’ll be honest, I’m a little overwhelmed by the response. Thank you. And for those of you asking what will happen — I’m kicking things off next week. Stay tuned.

With that out of the way, let’s dig in.

The Setup (Finding Asymmetry, Stacking the Odds)

Back in May of last year, I emailed Doug Casey. We need rare earths, I told him. Our portfolio didn’t have a single name in the space, and I thought that was a blind spot.

Now, rare earths had been coming together for a long time. As long as you’d been watching. And I’d been watching for the better part of a decade.

But over the past year it had kicked into another gear. A snowball was building. Take a look:

December 2024: China bans exports of gallium, germanium, and antimony to the U.S., retaliating against Biden’s semiconductor restrictions.

March: Trump responds by invoking the Defense Production Act to boost domestic mineral production.

April: China escalates, imposing export controls on seven rare earth elements, including high-performance permanent magnets.

Same month: Trump hits back with a Section 232 probe into critical mineral imports.

Each move triggered the next. By the time I sat down to write that email, the snowball was already rolling downhill.

But the macro case was only half of what made this a trade. The other half comes down to two things I always look for before I put money behind an idea.

The first is asymmetry. I want situations where the downside is limited but the upside, if you’re right, is several multiples of the entry price. Nassim Taleb, the risk analyst and author of “Antifragile,” calls this convexity. Think of it this way: you buy a stock at US$5. If the thesis doesn’t work out, maybe it drifts to US$3. You lose US$2. But if you’re right, it’s the kind of stock that can run to US$15 or US$20. You’re risking US$2 for a shot at US$10 or US$15.

Note: Here’s the beauty of asymmetric investing. Say you make ten speculative bets in a year. Six or seven go nowhere, maybe you lose a little on each. But the two or three that work return three, five, ten times your money. The winners more than cover the losers. You don’t need to be right every time. You just need the math on your side when you are.

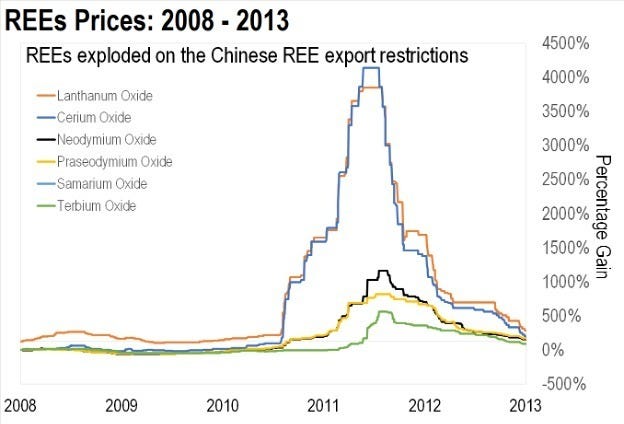

In rare earths, the asymmetry was staring you in the face. I knew that the last time China had seriously squeezed rare earth supply, back in 2010, when it cut off exports to Japan during a territorial dispute over the Senkaku Islands, prices went parabolic. Neodymium went from around US$40 per kilo to over US$300. Some elements spiked 10 to 20 times in under a year. Take a look at the chart below.

The setup was right there. I understood that even if a fraction of those 2010 gains repeated, the upside would be enormous. And most rare earth companies were still trading at low valuations. The market was treating the whole space as a niche trade, background noise to the AI frenzy.

But asymmetry alone isn’t enough. A lottery ticket is asymmetric — you risk US$2 for a shot at millions. That doesn’t make it a good bet. You need setups where the structural forces are working in your favor. I call it putting the odds on your side. And in rare earths, the odds were as good as any I’d ever seen.

Just consider the structural picture behind those policy moves:

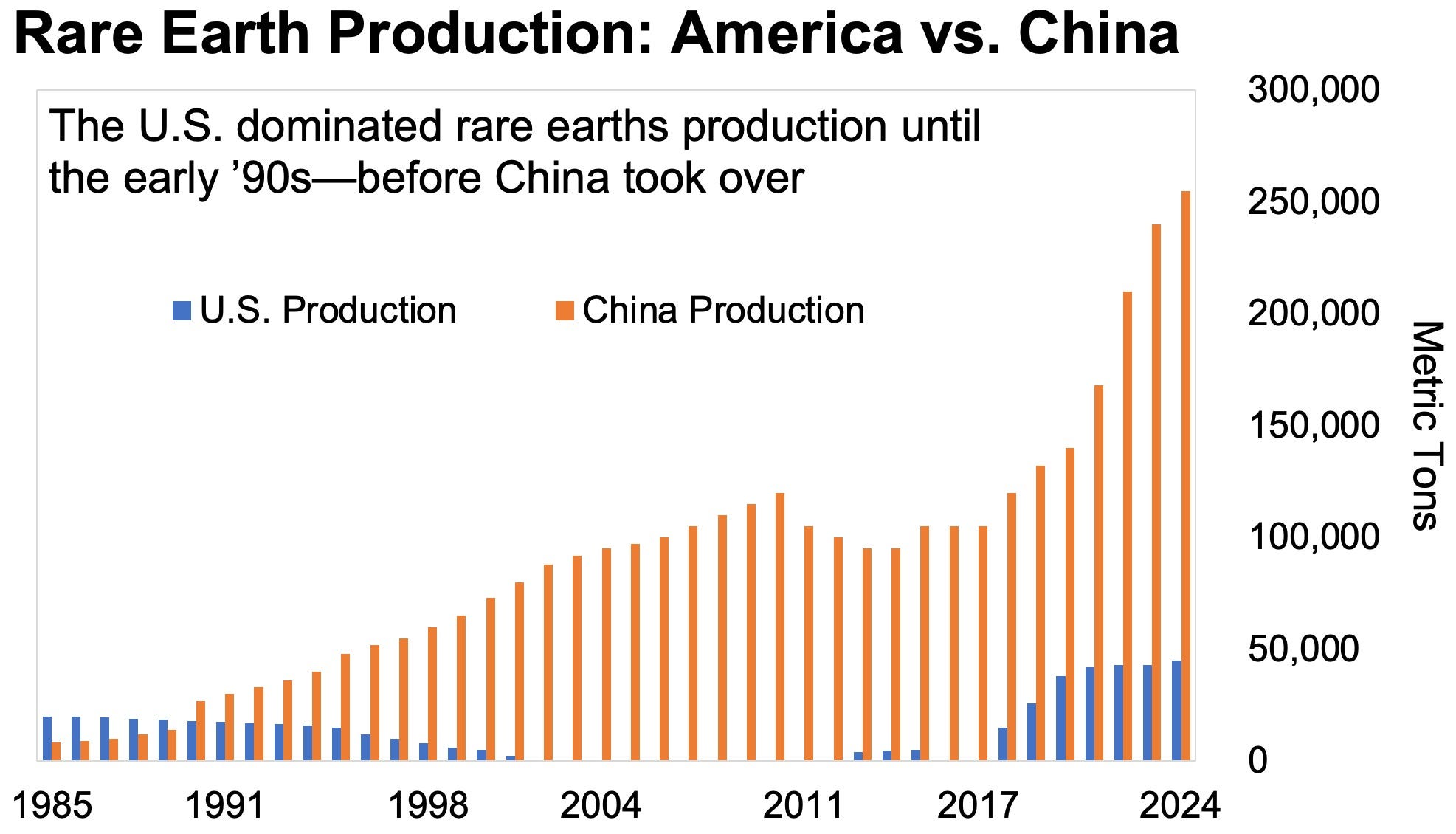

One country controls roughly 70% of global rare earth production and over 90% of refining — and was now restricting exports. That’s China.

The world’s largest economy and its largest military are utterly dependent on those materials. That’s the United States.

In fact, a report last year by Govini, a military analytics firm, put hard numbers on it: roughly 80,000 components across nearly 1,900 U.S. military systems contained Chinese-sourced minerals. 78% of all Department of Defense platforms. Navy: 92%. Air Force: 85%. Army: 70%. Javelin missiles, F-35 fighters, submarine sonar, drone guidance systems — all running on rare earths that came through China.

That’s what I mean by putting the odds on your side. It was clear to me that this setup meant the money was going to move. It was just a matter of time.

The Company

And I had the exact company to capture it: Energy Fuels (UUUU). What set it apart was a single asset: the White Mesa Mill in Utah.

To see why, you need to understand what happened to American rare earth production. Bear with me — this is the key to the whole trade.

Most people don't know this, but the U.S. used to be a major rare earth producer. It isn't anymore. Back in the 1980s and early '90s, U.S. miners routinely extracted rare earths as a by-product of iron and phosphate mining.

Note: Despite the name, rare earths aren’t that rare. They’re often found alongside other minerals in common ores.

Then came regulation. Citing nuclear proliferation risks, U.S. regulators threw rare earth processing under the same framework as uranium. The ores that contain rare earths, like monazite, come with small amounts of radioactive uranium and thorium mixed in. That meant the same licensing nightmare and the same sky-high compliance costs. So rather than deal with the regulatory burden, companies started burying the ore.

Within a few years, U.S. rare earth production shut down. China, which didn’t play by the same rules, kept processing. That’s a big reason it dominates the industry today.

Now here’s where Energy Fuels comes in. Because rare earth ores contain traces of uranium and thorium, you need a Nuclear Regulatory Commission (NRC) license to process them. That license is extremely difficult and expensive to get. Energy Fuels already had one. They’d been processing uranium at White Mesa for years, and they held the only active NRC license for a conventional uranium mill in the United States.

This meant that when they turned to rare earths, they weren’t starting from zero. They were plugging a new product into existing infrastructure, infrastructure that would take any competitor years and hundreds of millions of dollars to replicate. The uranium business was already there. The rare earths were the opportunity.

In 2024, they became the first American company in decades to commercially produce neodymium-praseodymium oxide, the stuff that goes into the permanent magnets used in EVs, wind turbines, and military tech.

Their breakeven cost was around US$30/kg. Market prices sat near US$60/kg. The margins were there. The feedstock was secured through joint ventures in Australia and acquisitions in Madagascar and Brazil.

So how did the same framework of asymmetry and odds apply at the company level? It was obvious to me that the market was still pricing Energy Fuels for its uranium business. The rare earth upside was essentially free, while the downside was pretty much capped by its functioning uranium operations. Remember, the margins were already there. And as for putting the odds on your side — well, that's what the only active NRC license in the country and existing infrastructure no competitor could replicate without years and hundreds of millions of dollars gave you.

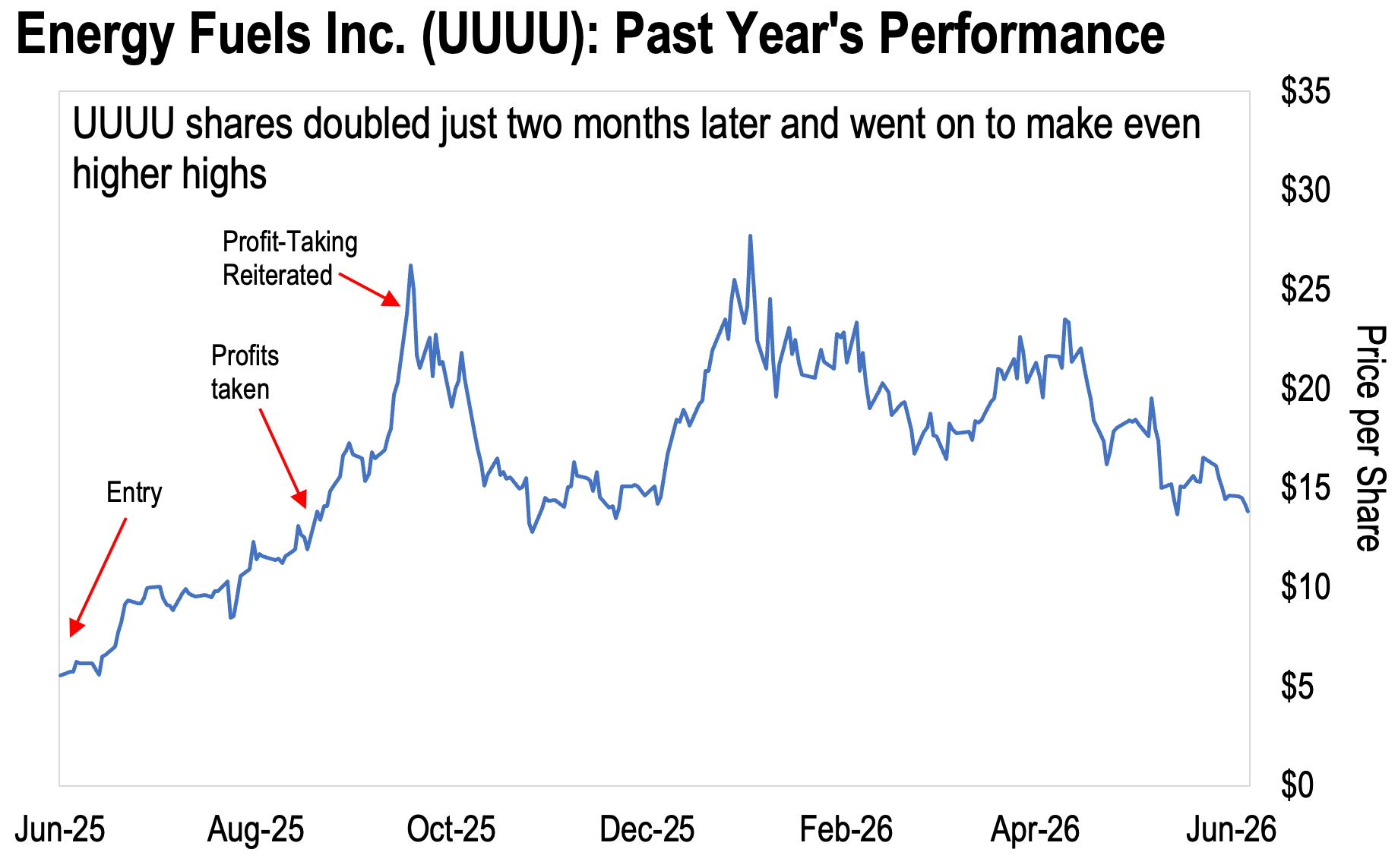

I recommended the stock in June 2025 at US$5.55. By August, the stock had doubled.

Two months. That’s all it took. Subscribers who followed the plan took their entire original investment off the table — the free ride approach I wrote about recently — and were playing with the house’s money from that point on. The position kept running. By year-end, it was up 160%. At its peak, over 400% — a five-bagger. (It's pulled back since, which is exactly why you take profits when you have them.)

The Bottom Line

The thesis is still very much playing out today. I mentioned that Energy Fuels was the first U.S. company in decades to produce NdPr oxide. Since then, they’ve added heavy rare earths — terbium and dysprosium — to the lineup at 99.9% purity. Meanwhile, in February, the Trump administration launched a US$12 billion strategic minerals reserve. And about two weeks ago, the Pentagon’s Office of Strategic Capital offered the company US$725 million in conditional financing to expand White Mesa.

Now, I wouldn’t normally walk through a trade from a paid publication. It wouldn’t be fair to the subscribers who paid for those picks. But the publication recently ran a discount marketing campaign — after I'd handed in my notice — that named Energy Fuels and cited the returns.

That said, the usual disclaimer applies. Past performance isn’t a guarantee. Your results will always depend on your own timing and execution. And again, I recommended this stock through a different publication. So here I’m showing you the process, not telling you to buy it.

And the process is the point. Finding asymmetry. Putting the odds on your side. Identifying the company with the edge. And taking risk off the table as the thesis plays out. That’s how I tend to think about these things. Let me know in the comments if this kind of walkthrough was useful. More next week.

Regards,

Lau Vegys

Thanks for this, Lau.

In your "what happened" essay you said:

"But over time, tensions started to build around what was being recommended, and how. I’d raise concerns. Sometimes they were heard. Other times they weren’t."

Can you share your real thoughts on HGRAF, now?

Appreciate you sharing the analysis and timing and the feedback in the comment section. Keep going. And stay in touch.