Europe's Recession Is Coming for America

The world's second-largest economy has ground to a halt. History says an ocean won't keep its troubles from reaching your wallet.

When I’m in Europe, I usually split my time between Lithuania and Spain. We leave for Spain in a few weeks, so I’ve been trying to make the most of Vilnius before we go. It’s a quietly beautiful, underappreciated city, the capital of what was once one of the largest states in Europe, with the history to match. There’s plenty to see.

But walking the same streets in the center most weeks, I’ve started to notice something. In the parts of town where the rents are highest and the foot traffic heaviest, more and more shopfronts are sitting empty. A café that was there last year, gone. A clothing store, papered over. And in one window after another, the same small sign: for rent.

It’s a little thing. Easy to miss if you aren’t looking. But once you start counting them, you can’t stop. Meanwhile, the economy seems to be catching up with the storefronts: the big Scandinavian banks that dominate Lithuanian lending, along with the country's own central bank, have all recently cut their growth forecasts for the year.

Now, you might be reading this from across the Atlantic, wondering why a few empty shops in Lithuania should matter to you. But here’s the thing: it isn’t just Lithuania. It’s the whole of Europe. And if history is any guide, Europe’s problems have a way of becoming America’s too. (More on that below.)

And if you look at the numbers, you can sense a storm gathering over economies that have, until recently, been limping along, propped up by little more than statistical mirages and out of control immigration.

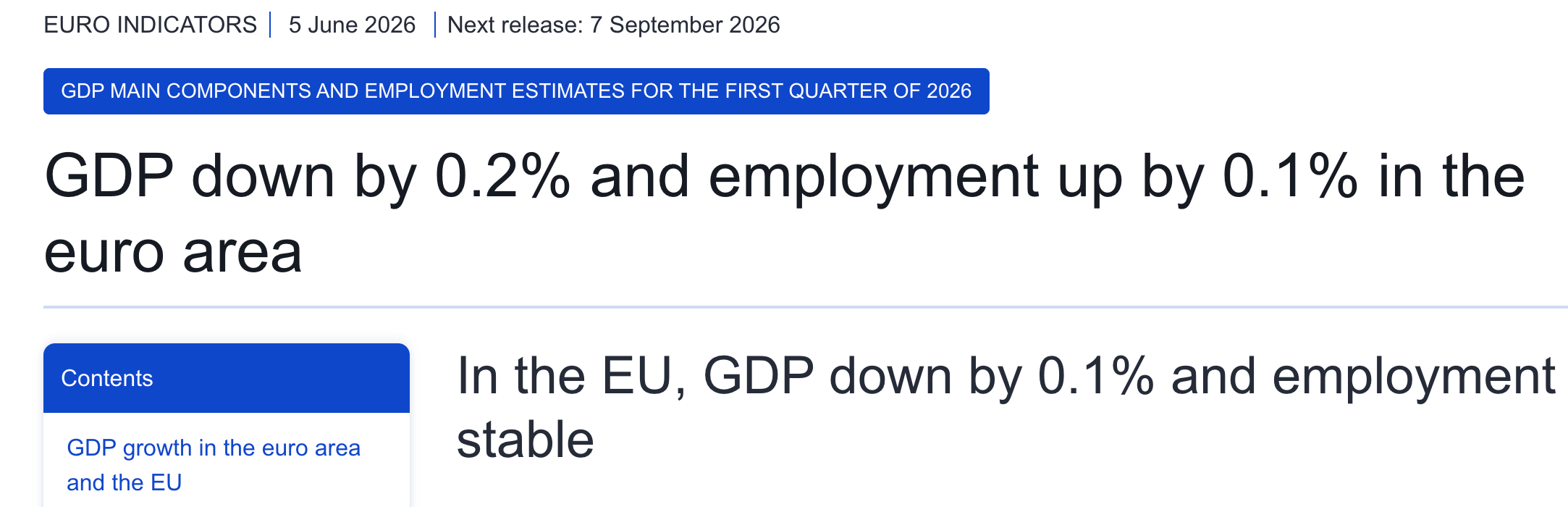

The latest figures tell the story. In the first quarter of this year, the European Union’s economy shrank by 0.1%. The eurozone, the 20 EU countries that share the euro, did worse still, contracting by 0.2%.

That doesn’t sound like much. But it’s the first time the bloc has gone backwards since late 2022, and it came in below even the modest growth the statisticians had first pencilled in.

Is that a recession? Technically, not yet. The textbook definition needs two consecutive quarters of contraction, and so far there’s only one. But consider the timing. That first quarter ended in March, before Iran, before the Strait of Hormuz was choked off, before oil started climbing and Europe’s energy bills climbed with it. All of that lands in the second quarter, the one we’re living through now. If Europe was already going backwards before the energy shock arrived, it’s hard to see the quarter that includes it coming out any better. A recession here isn’t the worst case. It’s the base case.

It's Ireland, Stupid

Pull the bloc’s aggregate number apart into the individual economies, and one culprit jumps out immediately: Ireland, a nation of five million people that accounts for ~3% of the EU’s output.

Irish GDP in the first quarter didn’t dip. It fell off a cliff, down about 12% in three months.

So what the hell happened there?

Short answer: President Trump’s tariffs.

The longer answer is more interesting, and to follow it you have to understand what Ireland’s economy actually is.

In simple terms, Ireland is where the world’s biggest drug companies park their profits. Pfizer, Eli Lilly, Novo Nordisk and the rest run enormous operations there, drawn by a low corporate tax rate and an accounting setup that lets them book a remarkable share of their global profit on Irish soil. That’s right: a huge slice of what Ireland counts as “its” economy is really just multinationals routing money through Dublin.

In normal times, that’s a wonderful trick. It pads the country’s GDP with profits earned all over the world and makes a small island look like an economic miracle. But these are anything but normal times.

To see what happened, rewind a year. When Trump began threatening steep tariffs on pharmaceuticals, those companies did the only rational thing: they raced to get their product into the United States before the tariffs could land. Over a few months they front-loaded tens of billions of euros of exports across the Atlantic. Irish exports to the U.S. jumped by more than half on the year. And because all of that gets counted as Irish output, Ireland’s GDP shot up more than 12% in 2025. On paper, it briefly looked like the fastest-growing economy in the developed world.

Fast forward to 2026, and the exports that had been pulled forward into last year simply weren’t there to repeat. The number that ballooned on the way up deflated just as hard on the way down.

Not Really Just Ireland

Now, the Irish story has real merit; no wonder so many EU officials have chosen to run with it. But it raises a question they would very much rather you didn’t ask: if a country of five million people, running 3% of the bloc’s output, can tip all of Europe into the red, what does that say about the other 97%?

Nothing good, that’s for sure.

Here’s the truth. The only reason Ireland’s reversal could move the whole headline is that there was almost no growth anywhere else to absorb it. The rest of the continent was already sitting at a dead stop. And that isn’t a one-off. Europe’s economic model has been quietly unraveling for years — a process that has only accelerated since the war in Ukraine.

To see how, you have to step back.

For decades, European prosperity rested on three quiet pillars:

Cheap Russian energy, which powered German industry, the one industry in Europe that truly matters.

The American security umbrella, which paid for Europe’s defense and freed it to build generous welfare states it could never otherwise afford.

Open foreign markets to sell into, a free-trading world happy to buy Europe’s exports, even as Europe kept its own market walled off behind tariffs and rules.

That was the deal. The problem is that all three are now all but gone.

Russia has been frozen out over Ukraine, and the cheap gas that ran German factories went with it. President Trump is pivoting to Asia and telling Europe, in no uncertain terms, to start paying for its own defense. And the open-trading world that once welcomed Europe’s exports is itself breaking apart, as Washington and others throw up tariff walls and retreat into rival blocs.

All of which leaves Europe exactly where it sits today: a continent that built its wealth on a world that no longer exists.

You can see it most clearly in Germany, the engine that was supposed to pull everyone else along. Earlier this year, German unemployment topped three million, the highest in over a decade. Since 2019, German industry has shed more than 340,000 jobs. Bosch, the auto-parts and appliance giant, is cutting 22,000. Thyssenkrupp, the old steel-and-engineering champion, another 11,000. Volkswagen’s quarterly profit fell by nearly a third. Foreign investment into Germany has now fallen for eight straight years, to a 17-year low. The country that was the backbone of the European economy has become its single biggest problem.

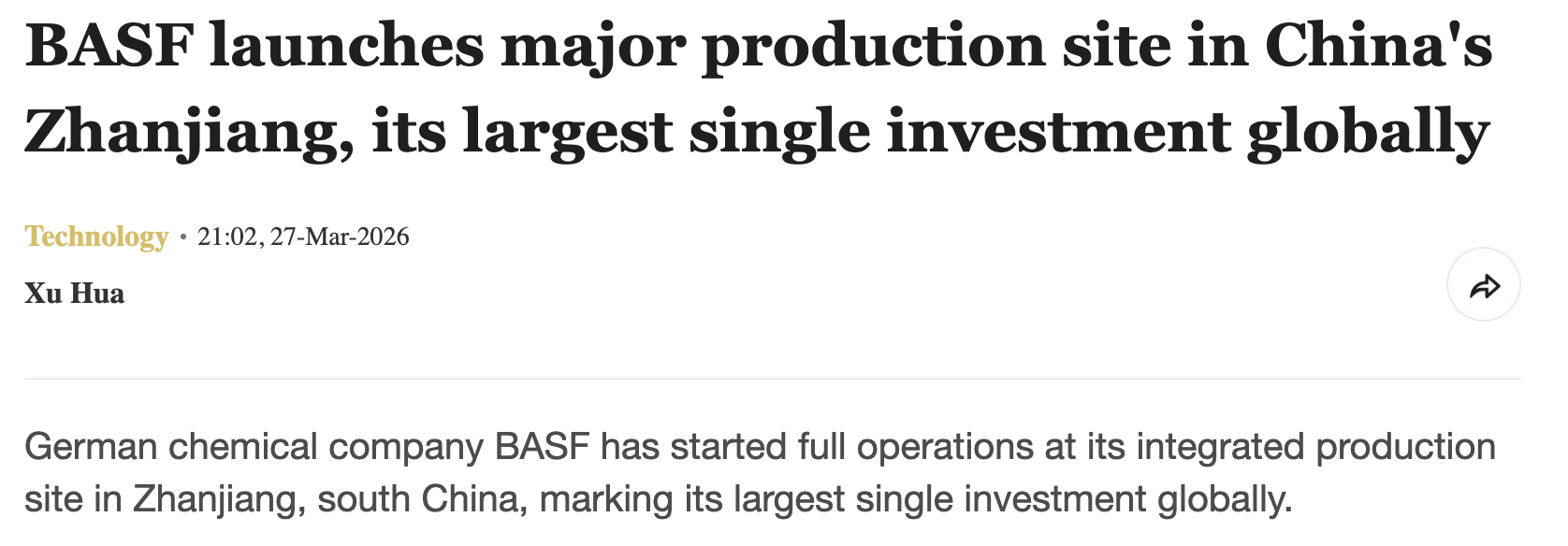

And, unsurprisingly, energy is a big part of why. European industry pays more than twice what American industry pays for electricity, and the war has only made it worse. So the factories are leaving. Between early 2024 and this year, more than a hundred chemical plants shut their doors in Europe. BASF, the German chemical giant that helped build the modern European economy, just opened the largest plant in its entire history. Not in Germany. In China. Ouch.

Worse, there’s nothing waiting to take their place. Europe hasn’t produced a technology company of global consequence in a generation. So far this year, the United States has minted dozens of new billion-dollar startups; Europe, barely a handful.

And here's another fact you may not know. As recently as 2008, the European economy was actually bigger than America’s. Today the U.S. economy is something like 40% larger, and it pulls further ahead every year. Measured per person, the average American now produces close to twice what the average European does.

Even Europeans aren’t buying the gleaming future their leaders keep trying to sell them. You don’t have to look much further than their bank deposits to see that. Something like €11 trillion (about $12.5 trillion) sits idle in European bank accounts earning next to nothing, money the EU’s elites have been dying to get their hands on, so far without success.

That’s more than the combined economies of Germany and France, because not even Europeans are confident enough to put that money to work at home.

When Europe Buckles

Now, again, you might read all this from across the Atlantic and shrug. Europe’s problem, not yours. And most days, fair enough. Americans don’t wake up worrying about Brussels, nor should they have to. America has plenty of problems of its own.

But here’s the thing, and like I said at the top: Europe’s problems have a way of becoming America’s problems. (And you don’t have to reach all the way back to World War Two to see it.)

Consider this.

The European Union is 449 million people and around $20 trillion in output, the second-largest economy on the planet after the United States. The two are also each other’s biggest trading partners, with nearly $2 trillion in goods and services crossing the Atlantic every year. Together, they account for almost half of global GDP.

So what happens when an economy that size stalls?

We don’t have to guess, because we watched it happen not long ago. During the eurozone debt crisis of 2011 and 2012, a wobble in Europe nearly dragged a fragile American recovery — still finding its feet after the 2008 financial crisis — back into recession. The chain ran like this:

European demand dried up → American exporters lost one of their biggest customers.

Money fled the euro into the dollar → the stronger dollar made every American export pricier and harder to sell.

European banks, loaded up on their own governments’ shaky debt, started to buckle → and because banks on both sides of the ocean lend to one another constantly, those losses landed on American balance sheets too.

As a result, American hiring stalled through the summer of 2011, the stock market lurched through stomach-churning swings, and the Fed fired up yet another round of stimulus to “steady things.” U.S. growth slumped from 2.7% in 2010 to 1.6% in 2011, and the IMF kept cutting its U.S. forecasts as the crisis across the Atlantic dragged on.

Not because anything had broken in America, mind you, but because something had broken in Europe.

Now, to be fair, the U.S. is in a far stronger position than Europe. It has plenty of advantages, but the one that matters most right now is energy. America is the world’s largest producer of both oil and natural gas, a net energy exporter, and now the top LNG supplier on earth. Whatever it needs, it can pull out of its own ground, with plenty left over to sell.

Europe is the mirror image. It imports close to 60% of its energy, and for years it has gone out of its way to make that worse, Germany shutting its last nuclear plants in the middle of an energy crisis, the bloc sitting on its own gas and betting on the weather instead. So when oil and gas get more expensive, there’s no cushion at home to soften the blow. There’s just the bill.

So on this alone, the two are not in the same boat. Not even close.

But energy independence is not trade independence. The eurozone debt crisis showed as much.

They say that when America sneezes, the rest of the world catches a cold. True enough. But it runs the other way too: when Europe buckles, America feels the tremors. And this time, they could be stronger. Back in 2011, America was climbing out of a crisis with room to maneuver. Today it’s carrying a record national debt pushing toward $40 trillion, an interest bill that now runs higher than its entire military budget, and rampant inflation. A stalling Europe leaning on all of that is the last thing America needs.

And believe me when I tell you: Europe’s hard times are only getting started. I’ll be reporting more on it from Spain in the weeks ahead.

Regards,

Lau Vegys

Sadly, Europe is done. Years of socialism and, now, repression of everything that does not involve the government rulings, has taken away the spark and the cultural differences that made each country delightful to visit. Glad I saw it when! I do not care if I ever visit Europe again.

Americans are tired of supporting other countries. I never was an isolationist, but now it sounds like a good idea. Under Biden, the amount of illegals, so-called “migrants” and criminals entered our gates in the thousands. The same in Europe. Until people stand on their own feet, work, and break free from the idea that the governments of the world owe them everything for free…all countries are at risk. European leaders peddling “social justice” do not even know what they are talking about. Yes, it is happening here, as well. Over- regulated businesses can not stay open. Look at the Covid-19 debacle. That almost destroyed America.

Thank you for the good article. , Lau! Enjoy your travels, and stay SAFE!

I agree with this fine article on everything although when it comes to defense spending the free ride given to Europe during the cold war should have ceased in 1991 and along with it NATO. The war in Ukraine was a result of the continued existence of NATO and US neocon, State department and Administration influence and interference. The pushing by the west has put Russia in the same camp as China which could have been avoided but now the EU is obsessed with Russia as a last desperate deflection/distraction from their green theocracy (and central planning) responsible suicidal economic decline.