America's Coming Dollar Devaluation

There's only one way out of $39 trillion in debt

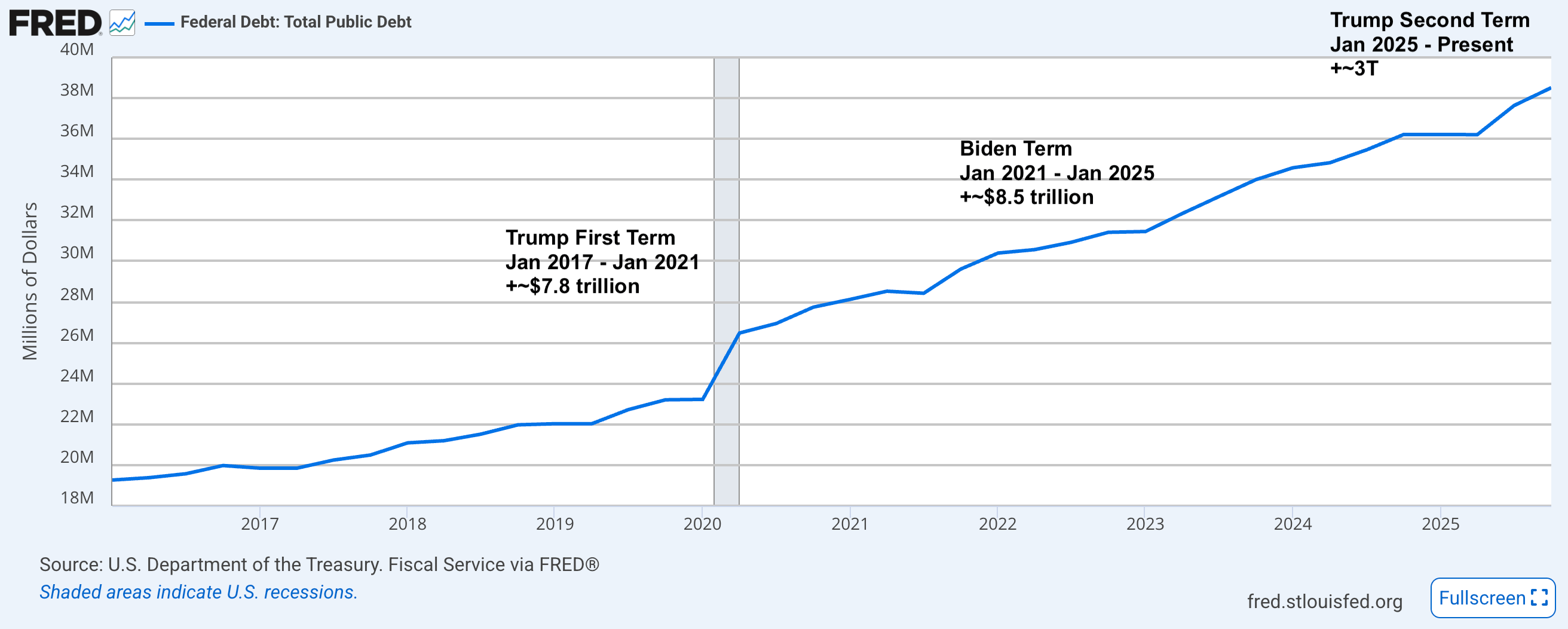

When Donald Trump first took office in January 2017, the national debt stood at $19.95 trillion. He promised to eliminate it — not reduce it, eliminate it — within eight years.

Today it’s $39.2 trillion. It nearly doubled.

Now, a big chunk of that happened under Sleepy Joe. Roughly $8.5 trillion worth. COVID stimulus, a $1.2 trillion infrastructure bill, the Inflation Reduction Act, the CHIPS Act, repeated student loan forgiveness attempts, and the usual Washington math.

Still, Trump returned to office last year and, instead of even attempting to make a dent in it, let alone eliminate it, he has piled on another $3 trillion.

The reason is simple: spending. Trump has never been shy about spending big.

So where is all that money going? A lot of places. His “One Big Beautiful Bill” alone adds $3.4 trillion to deficits over the next decade. (Remember: deficits become debt.) But a good chunk of it comes down to Trump’s newfound fascination with war and playing the world’s policeman, which is quite something if you remember all the campaign rhetoric about ending wars and bringing the troops home.

I won’t dwell on the hypocrisy. Point is, war is expensive.

The Iran war alone has already cost $25 billion. And that’s just the start. As I write this, the Pentagon is floating a $200 billion supplemental war funding request that can’t find enough votes in his own party. That’s to say nothing of his FY2027 budget ($1.5 trillion for the military, the largest request since the Cold War) to build what he calls a “Dream Military.”

We’re talking a new class of battleships, autonomous weapons systems, expanded nuclear modernization, and a homeland missile shield called the “Golden Dome” — essentially an Iron Dome for the entire continental United States, which the Congressional Budget Office estimates could cost up to $1.2 trillion over twenty years. The military-industrial complex must be rubbing their hands.

Nobody Was Ever Going to Fix This

Now, I realize that when you hear “national debt of nearly $40 trillion,” your eyes glaze over. It’s such a mind-boggling amount that it’s hard to even comprehend how big it actually is. So let me try to bring it a little closer to home.

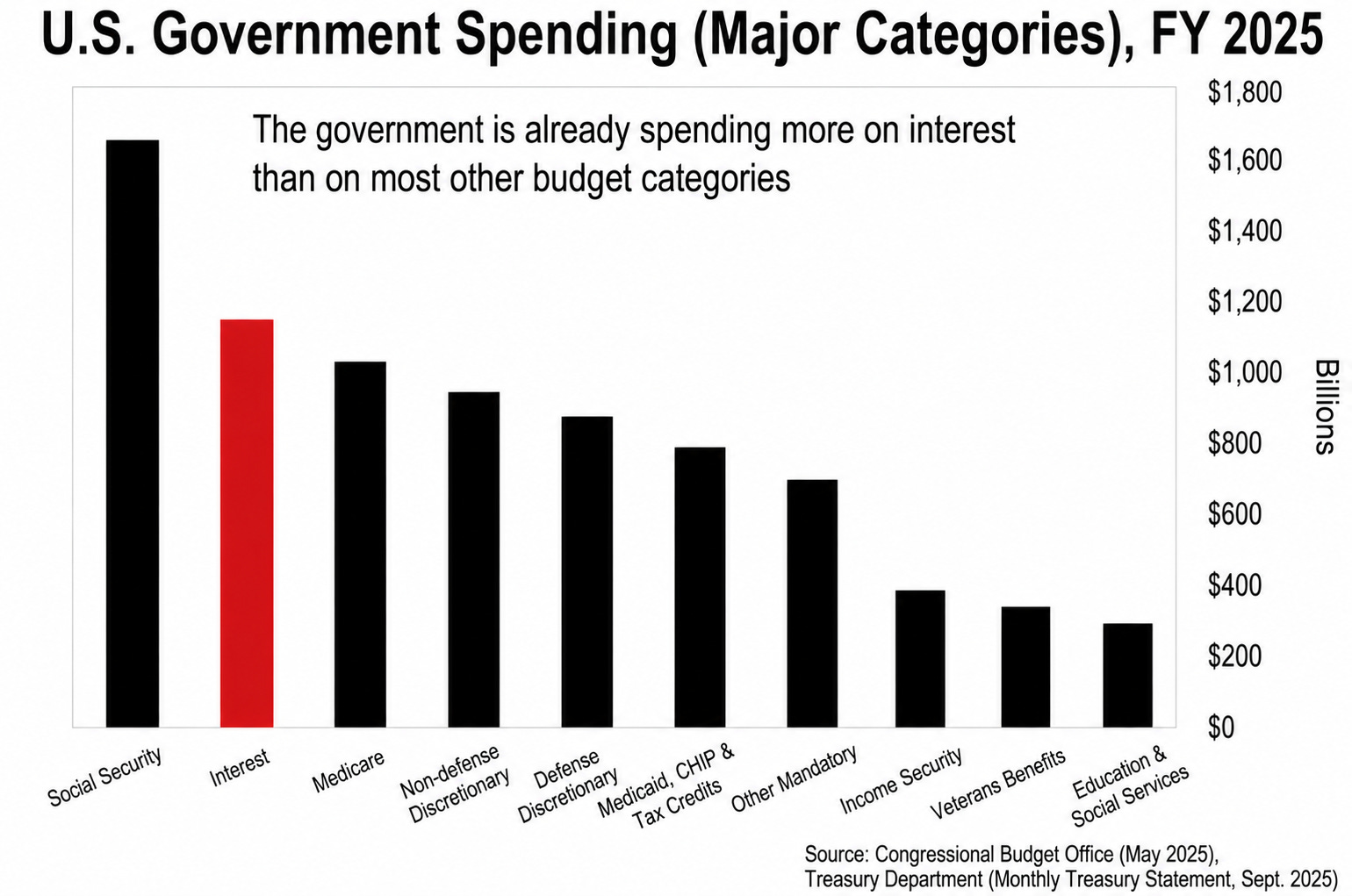

Enter interest expense. This is the number the government has to pay on all that debt — because debt is never free. It’s never just principal. It’s also what you owe to those kind enough to lend you the money. And in the case of the U.S. government, it’s staggering. Interest on the national debt has crossed $1 trillion a year. That’s $3 billion every day. Interest now costs more than the entire military budget. More than Medicare. In fact, the only program that costs more is Social Security.

Here's why this matters. Interest is the one bill Washington can't cut or skip, and it feeds on itself: with no spare trillion lying around, the government borrows to pay the interest, which only swells next year's bill. A snake eating its own tail. Worse, most of this debt is short-term, rolled over at whatever rate the market demands. So if rates climb — and with inflation hot and the 30-year already through 5%, they may have to — the bill doesn't drift. It jumps.

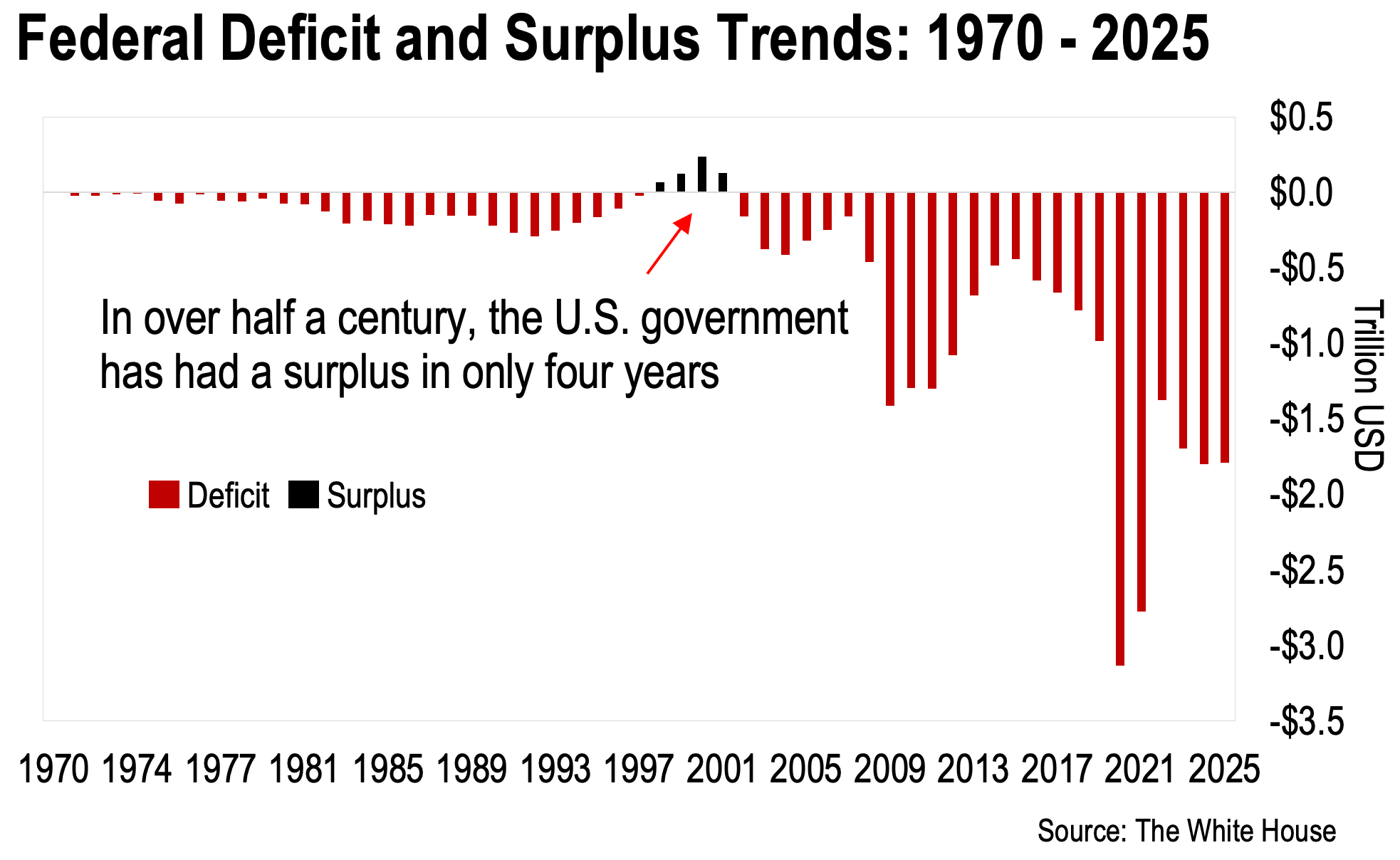

Now, before I get to how this ends, let me make something clear. This isn’t a Trump problem. It’s a systemic one. Every politician, red or blue, has the same spending habit. Because if there’s one thing the federal government has been perfectly consistent about, it’s spending more than it takes in. Over the past 76 years, it has run a deficit in 67 of them.

And it's gotten worse, not better. For the last 24 years straight, Washington has overspent every single year, piling on more debt each time. It genuinely doesn't matter who's sitting in the White House — Bush, Obama, Trump, Biden, Trump again — every one of them breaks the last guy's record.

Note: The last “balanced budget” under Bill Clinton was largely the result of accounting smoke and mirrors, and the debt still increased during that time.

The point is, it doesn’t matter which party is in power. The budget isn’t getting balanced, and the debt keeps rising.

It bears repeating because I was always amazed by how many otherwise sensible, fiscally conservative people swallowed Trump's promise to wipe out the debt in eight years. Hook, line, and sinker.

It Can't Be Balanced

Just how bad is it?

Consider this...

To balance the budget today, you’d have to cut spending by around $2 trillion a year. For context, the entire Social Security program costs roughly $1.7 trillion a year, and the military budget runs close to $1 trillion. Even eliminating either completely wouldn’t be enough.

Put yourself in a politician’s shoes. Imagine stepping up to the microphone: “My fellow Americans, we need to slash government spending by $2 trillion a year. We’ll start by cutting Social Security payments...” You wouldn’t finish that sentence before being booed off stage, assuming you made it past your campaign donors.

More realistically, balancing the budget would require across-the-board cuts of 30-40% to all non-debt-service spending. That means ~40% less for Social Security’s beneficiaries, Medicare, veterans’ benefits, military spending, education, and infrastructure. No politician who wants to remain in office would propose this. Even if they did, Congress would never pass it.

But, for the sake of argument, let’s imagine the government does the unthinkable: cuts spending massively while the Federal Reserve stops printing money.

This would trigger deflation and economic depression, causing the price of everything to plummet: stocks, real estate, private equity investments, all assets.

And who owns the majority of these assets? The ultra-wealthy.

I’m not talking about your average millionaires or even multi-millionaires here. I’m talking about the Jeff Bezoses and Jamie Dimons of the world, the Wall Street financial elites, the politically connected class that has benefited from decades of easy money policies.

Their fortunes are tied up in assets that have skyrocketed in value due to the Fed’s money printing and the resulting inflation. That’s why the top 1% now hold more than ten times the wealth of the entire bottom half.

The last thing these people want is to see the value of their assets deflate like a birthday balloon the morning after. And that’s exactly what would happen during an economic depression.

Sure, some wealthy individuals might relish the chance to scoop up assets on the cheap, but the politically connected elites would never back policies that would shrink their net worth to a fraction of what it is now. That’s their worst nightmare.

The “Easy” Way Out

History shows that when governments face tough choices, they almost always take the path of least resistance. Cutting spending is politically toxic. Default is off the table. But gradual devaluation? That’s always the preferred stealth option.

It allows politicians to:

Avoid explicit spending cuts.

Continue funding popular programs.

Maintain the appearance of “doing something” while avoiding blame for direct cuts.

Preserve their power and wealth.

Devaluation is also essentially a get-out-of-debt card for the government because it reduces the real value of what it owes.

Let me give you a simple illustration that hits close to home...

Say your family has a fixed $400,000 mortgage, roughly the average house value in the U.S. right now. If high inflation hits and prices across the economy rise dramatically (say your and your partner’s salaries double or triple along with most prices) that $400,000 debt suddenly feels much lighter. While your mortgage payments stay the same, they become a smaller portion of your growing income.

The government’s massive debt works the same way: inflation shrinks the real value of their $39.2 trillion debt burden while tax revenues rise with inflation.

The elites benefit too. During inflation, asset prices soar… stocks, real estate, private equity investments all rise in nominal terms.

The pandemic years proved this dramatically: The number of U.S. billionaires grew from 614 to 737 between March 2020 and March 2024, while their combined wealth surged by around 90% to about $5.53 trillion. Not coincidentally, this happened when the Fed ramped up money printing to unprecedented levels.

The bottom line: the path of least resistance is a win-win for those in power and the elites. For the majority of Americans? Not so much.

One Way or Another

Now, it’s no secret that Trump has made a weaker dollar an open goal. He thinks a cheaper dollar gives American factories a leg up, and he’s never hidden it. The dollar has already slid more than 10% since he took office, its worst run in over half a century, and his reaction was, “I think it’s great.”

But even if it weren’t Trump, the point would still stand. When countries become financially unstable, they reach for currency devaluation over outright default or austerity. From Weimar Germany to modern Venezuela, the playbook never changes.

Why should the U.S. be any different? Because it’s a developed nation? Tell that to 1970s Britain.

Note: In 1976, the U.K., then one of the world’s leading economies, was forced to go hat in hand to the International Monetary Fund (IMF) for the largest loan the IMF had ever granted. The British pound had collapsed, inflation was running at 27%, and the government couldn’t sell its debt. Being a developed nation didn’t protect them from the consequences of fiscal mismanagement.

Now, I’m not here to scaremonger. I want to be realistic… I don’t think the dollar goes overnight.

It didn’t happen overnight under Nixon, either.

But in just ten years, it lost over half its purchasing power. Today, that same dollar buys about 90% less than it did in the early 1970s. I think history repeats itself here, only faster. And the accelerant is AI. As I wrote last week, it’s going to put tens of millions of people out of work, and when it does, the government will respond the only way it knows how: with checks. Transfer payments, then some flavor of universal basic income (UBI), all of it funded by the printing press. Point is, we won’t have the luxury of decades this time around.

Trump or not, make no mistake: devaluation is coming.

Regards,

Lau Vegys

You describe with admirable clarity what you mistake for a prediction. It is not a prediction. It is a diagnosis already rendered, decades ago, by anyone who understood that inflationism is not an accident of policy but its very essence under fiat money.

You write that “devaluation is coming.” I must correct you: devaluation arrived the moment the link to gold was severed. What you anticipate is merely the acceleration of a process long underway. There is no means of avoiding the final collapse of a boom brought about by credit expansion. The alternative is only whether the crisis should come sooner, as the result of a voluntary abandonment of further credit expansion, or later, as a final and total catastrophe of the currency system involved. Your government, like all governments before it, has chosen “later.”

You are correct that no statesman will propose the necessary retrenchment. But do not flatter the politicians by calling this cowardice. It is something worse: it is the logic of interventionism itself. Each intervention creates the conditions that seem to demand the next. The deficit demands the debt; the debt demands the cheap money; the cheap money demands the next deficit. The interventionist state is not failing to balance its budget — it is constitutionally incapable of doing so, for its entire claim to legitimacy rests upon distributing what it has not earned.

You note that the wealthy and politically connected profit from the inflation. Just so — this is no novelty. Inflation is never neutral. It enriches those who receive the new money first and despoils those who receive it last: the wage earner, the pensioner, the saver — precisely those virtuous citizens whom the demagogue claims to champion. Inflation is the fiscal complement of statism, and it is the most insidious of all taxes, for it is levied without legislation and blamed upon the grocer.

Where I must caution you is in your fatalism. You say the playbook “never changes.” But the playbook is not a law of nature; it is a choice made by men who hold false ideas about money. Sound money is not a technical arrangement. It belongs in the same class with constitutions and bills of rights — it is an instrument for the protection of civil liberties against despotic inroads by government. If the public again comes to understand this, the printing press can be stopped. If it does not, then your forecast requires no economist to confirm it. The masses who applaud each new “stimulus” will learn, as the Germans of 1923 learned, that the government cannot make all people richer by making the money poorer.

The question is not whether the bill comes due. It is only who shall be made to pay it, and whether anything of the market economy — which is to say, of civilization — remains when it does.

It doesn’t have to be this way. Or does it?

I would contend that it is impossible for the United States to have both a balanced budget and the world’s reserve currency. It is the US Dollar that runs the world.

If the US were to have a balanced budget, then there would be no increase in wealth around the world (in nominal terms), because every liability of the US government is someone else’s asset. The years when the US had a balanced budget (in the post-World War 2 era) were always lea-in’s to a recession in the US. And it is true that under Austrian Economic Theory, recessions were the cleansing of the excesses of the last expansion. But, for worse or worse, we aren’t living under that type of system, where the world revolves around economic balance. Instead, it revolves around credit. And the US is the biggest abuser of credit on the planet. But it’s that credit, extended to the US, that is responsible for all the (phony) wealth on the planet.

Now, any politician voting for a recession would find a new home on the sidewalk (which is probably a good thing). But if the US Dollar is going to maintain its status in the world’s banking system (which isn’t certain), the political class in Washington, DC will do their damnedest to prevent a recession. Which means they will never balance the budget.