Yes, AI Will Probably Take Your Job. It Will Probably End the Middle Class Too.

Why your work might be going the way of the horse—and how to be on the right side of what comes after.

A quick note before we dive in. Today’s piece is longer than usual. It’s also more ambitious than usual — I’m trying to thread three different stories that I think are actually one story, and you’re going to need all three to see the whole shape. So bear with me. If you only have a minute, the headline is the thesis. If you have ten, the rest of it will, I hope, be worth your time.

So a few weeks ago, Meta (the parent company of Facebook) told roughly 8,000 people to work from home for the day. Then it fired them by email. That was about 10% of the company.

Here’s the thing. Meta wasn’t in trouble. The stock was near records. This wasn’t a company cutting muscle to survive a bad year. It was a company quietly shifting its money away from people and toward machines. Eight thousand gone, seven thousand survivors reshuffled into new AI divisions, and that’s to say nothing of the 6,000 open jobs they just quietly left unfilled.

While all this was going on, Mark Zuckerberg was reportedly aboard his $300 million super yacht somewhere in the Mediterranean.

Now, Meta isn’t an outlier. American employers announced about 1.17 million job cuts in 2025, the worst year since the pandemic, and tens of thousands of those were attributed to AI directly. And that’s just the layoffs, which tell only half the story.

The other half is the hiring that never happened. Announced hiring plans fell by a third last year, to the lowest level since 2010. In other words, companies are quietly deciding that the next worker simply won’t be needed.

Now, point any of this out to anyone in the tech world (or in the government, for that matter), and you’ll get a version of the same response. It goes something like this: “Don’t worry. Every wave of innovation gets predicted to destroy work. And every wave ends up creating more jobs than it destroys.”

And look, I get it. This response isn’t wrong on the historical record.

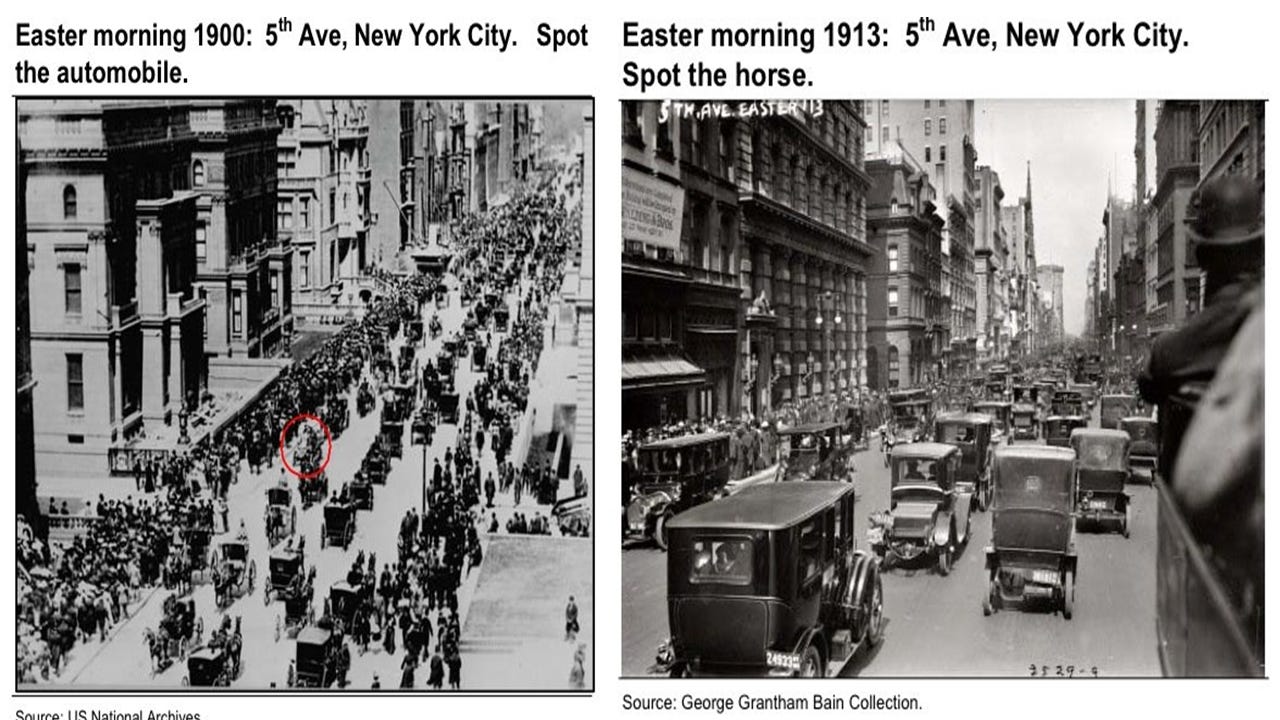

The first industrial revolution (Britain, late 1700s) gutted skilled hand-weavers. They smashed the looms in protest. Called themselves Luddites. We pretty much use their name today as a synonym for fool. Because within a generation, the mechanized cotton mills had hired millions more people than the hand-weavers ever employed.

The tractor (early 1900s in the U.S.) put almost half the country’s farm labor out of work. In 1900, roughly 40% of Americans worked on farms. By 1970, that figure was under 5%. Those farmhands didn’t starve. They moved to cities and built the postwar manufacturing economy that defined the American Dream.

The assembly line (Ford, 1913) replaced the master craftsman who built a car bumper to bumper. But it also created the factory job that became the spine of the American middle class for the next fifty years.

The spreadsheet (VisiCalc in 1979, Excel in 1985) ate most of the country’s bookkeepers and clerks. In their place came the entire knowledge-work sector — tens of millions of jobs (at least until AI showed up to eat it).

The internet (mid-1990s onward) vaporized newspapers, travel agents, video rental stores, encyclopedia salesmen, half the music industry, most of the postal service’s volume, and a long tail of jobs nobody remembers anymore. But it also built every tech company that now dominates the S&P 500.

So yes, every previous innovation eventually created more jobs than it destroyed. The Luddites, in the long run, were always wrong. So why would this time be any different?

Yes, It Is Different This Time

Now, I want to be careful here. I’m not buying into the whole AI-doom thing. I think the future is going to be amazing in many ways. Cheaper goods, longer lives, scientific breakthroughs, the works. But to actually reap the benefits of that future, you have to be one of the people on the right side of the transition. And unfortunately, I think most people won’t be. Most will either fall by the wayside entirely or end up dependent on a government check (more on that in a moment). Which means if you don’t want to be one of them, you need to think realistically about how this thing actually unfolds.

And to do that, you have to be clear-eyed about one thing first. The AI revolution is a fundamentally different kind of animal from every previous wave on that list above.

You see, every previous machine moved human labor somewhere new. The mechanized loom needed a mill worker. The tractor needed a driver. The assembly line needed an operator. The spreadsheet needed an analyst. Each tool needed a human attached to it to be worth anything. Productivity went up for the worker, and the worker got paid for the gains (well, more or less — more on that in a minute too).

AI is the first technology designed for the opposite purpose. It isn’t built to make your labor more productive. It’s designed to make your labor unnecessary.

There’s a useful analogy for this. Not a human one, but a useful one. Think about horses. Before the internal combustion engine arrived, horses were arguably the most important factor of production in the entire American economy. The U.S. horse population grew roughly fivefold between 1840 and 1900, to over 21 million animals. Then we built tractors and automobiles. Within thirty years, horses were obsolete. They didn’t get retrained. They didn’t move to better jobs. They just stopped being needed.

If current AI deployment trends hold up, there’s a very good case to be made that humans, in economic terms, will go the same way as horses. To be clear, I’m not predicting anyone gets sent off to the glue factory. But economically? Same arc.

Note: Yes, AI will create some new categories of work: prompt engineers, AI trainers, model evaluators, that sort of thing. But the trouble is, those new categories are themselves AI targets. They collapse into themselves rather than expanding into real headcount. The new jobs AI creates tend to be the next jobs AI eats.

Now, I’m not a Luddite, and I don’t have a problem with AI as a technology. For better or worse, it’s just the logical progression of human achievement, the kind of thing that would have emerged sooner or later. We’re a species that improves things incrementally until we don’t need to do them anymore.

OK, so how many people are we actually talking about? That depends on who you ask, of course, but one thing is clear: the numbers aren't small. Goldman Sachs reckons roughly 300 million jobs globally are exposed to automation by AI. The U.S. and other developed economies take the brunt of that. Call it conservatively 70 to 80 million American jobs in the “exposure zone.” McKinsey, separately, estimates that about 12 million Americans will need to switch career categories entirely by 2030. That’s in less than four years. To put that in perspective, that’s roughly a hundredfold acceleration on the AI-attributed pace today. And that’s the consultant version. Not the doomer one.

Speaking of the doomer reading, Anthropic’s CEO Dario Amodei has said publicly he thinks AI could wipe out half of all entry-level white-collar jobs within five years. Geoffrey Hinton (basically the godfather of modern AI) has been warning about the same thing for two years now.

Assume the truth lands somewhere in the middle between the doomers and the consultants. That still raises the obvious question: if you fire all the workers, who buys the product?

It’s a fair question. Labor income isn’t just a corporate cost. It’s also demand. The economy is a two-way street. Hollow out labor and you risk demand collapse. What’s the point of fatter margins if there’s nobody left to buy what the AI-driven industries are producing?

Enter the almighty state.

The state will not allow demand to implode. It would be devastating for the economy, and most of all devastating for the wealth of the people who actually run the show. So the state will backfill the gap. Larger deficits. More transfer payments. Eventually, some flavor of universal basic income (UBI), financed in the end by the central bank and its money printer.

Mind you, we already got a preview of how this works during COVID. In the U.S., the government literally mailed checks directly to households — the $1,200 stimulus payments, then $600, then $1,400 — on top of expanded unemployment that paid more than many people’s old jobs did. Spain rolled out a permanent minimum-income guarantee during the same period. (And Finland had run a literal UBI pilot only a few years before.) In short, COVID was basically the dress rehearsal. The state learned that direct cash transfer to households at scale actually works. All that’s needed now is the next excuse to do it again.

The End of the Middle Class

So who wins in this arrangement?

Well, the biggest beneficiaries are clearly the AI-era equivalent of the old industrial barons. Call them the AI aristocracy — the tiny class that owns the systems doing the work everyone else used to do. In addition to fatter margins going straight to their bottom line, they’ll also have a captive customer base (because the state will be funding everyone’s grocery bill) and political cover, because they’ll be the only people building anything anymore.

Well, what about the rest of the population? They’ll no doubt end up increasingly dependent on a state check to function, making them docile and subservient as a result. Which is, conveniently, exactly the kind of population politicians have always preferred to govern.

You don’t need to be a conspiracy theorist to notice what this system actually is. The textbook name for the fusion of corporate and political power is corporatism; or, if you prefer the more candid synonym, fascism. Italy’s Benito Mussolini reportedly used the two terms interchangeably.

Now, if you think this sounds like a dystopia that’s still many decades away, here’s the part you might be missing. The process has been running for fifty years already. Let me show you.

Wind the clock back to August 15, 1971. On that day, President Nixon killed the last remnants of the gold standard.

Note: I say “remnants” because the U.S. had already left gold for domestic dealings back in 1933. Non-U.S. people and governments could still exchange dollars for gold at the U.S. Treasury, but by the late 1950s, even that was reduced to only foreign central banks. That was the last discipline against unlimited money printing.

Now, I’m not saying Nixon somehow devised this to bring about the AI future fifty years later. Of course not. But the move turned out to be the logical first step in the long march toward the kind of system I just described. Because you cannot run an economy where a tiny aristocracy owns the machines and the state writes checks to everyone else, without unlimited money printing. Gold-backed money is a hard constraint on state spending. Fiat money isn’t.

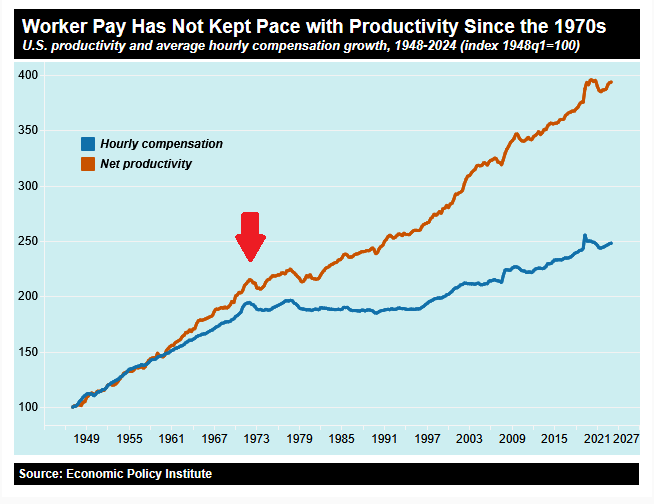

Now, guess what happened to the American middle class once that constraint came off? It started to slowly come apart. Take a look at the chart below — it shows what happened to American productivity and wages after Nixon took the brakes off.

As you can see, for about 25 years after World War II, productivity and worker pay moved in lockstep. The harder Americans worked, the more they earned. That was the golden age of the American middle class. A single income could buy a house, a car, send the kids to college, and fund a retirement. Wages, adjusted for inflation, rose alongside productivity.

Then 1971 happened. The two lines diverged. Productivity kept climbing. Real wages flattened. The graph above clearly shows how the real wages of the average American have essentially remained stagnant since the early 1970s.

Now, you might ask — how is any of this relevant to today?

Well, let’s look a little deeper. In 1970, wages made up about 52% of total U.S. national income. By the early 2020s, that share had fallen to roughly 43%. A 17% drop in fifty years. And the trend hasn’t stopped — by my rough guess, the figure today is somewhere around 40%. Do you see where this progression is going?

Right, but you might be thinking, the dollar has been fiat for over five decades. There’s no more gold standard to remove. The damage is done.

Not quite. The damage is just entering its second phase.

Enter the CBDC.

Now, I don’t know if it ultimately ends up being a pure central bank digital currency by 2030 (the date the current legal prohibition sunsets, if you read my recent piece on it), or a privately controlled equivalent run through dollar stablecoins like USDC and USDT, or some combination of the two. What I do know is that it will be fiat on steroids. Programmable. Surveilled. Fully wired into the state’s spending machinery.

It will also make money printing operationally much easier. Today, when the Fed wants to inject liquidity, it has to work through the multi-layered banking plumbing. It’s sometimes slow, frictional, politically visible. A digital dollar cuts straight through that. With the rails running direct between the central bank and the end user, the printer goes from slow tool to near-instant one.

Bottom line: the digital dollar is what makes UBI possible at scale. Managing the AI transition will require trillions of new dollars flowing every year, on demand, with no “political accountability” slowing it down. The current banking system would break under the load. A programmable digital dollar can do it before lunch.

What to Do About It

OK, so where does that leave you?

Look, when I said earlier that the future is going to be a small AI aristocracy and the rest of us as state-dependent consumers, that was a bit of a simplification. Some people will survive as something resembling middle class. That’s how it worked the last time, too. The American middle class didn’t disappear after 1971. It survived. But it survived by leaning on four workarounds that hadn’t been necessary before. And it’s worth going through them, because they give us a pretty clear hint about what’s going to be needed to survive what’s coming.

Two-earner households. Pretty quickly, one income stopped being enough to maintain a middle-class lifestyle. So the wife went to work. Couples doubled their labor hours, called it progress, and convinced themselves nothing structural was wrong.

Rising household debt. When wages don’t rise, you borrow. Credit cards. Student loans. Ever-larger mortgages on ever-more-leveraged homes. Total household debt in America has roughly tripled in inflation-adjusted terms since the 1970s.

Home equity appreciation. The one asset that most middle-class families actually owned, far and wide. The one place where post-1971 monetary debasement worked in their favor instead of against them.

Owning assets. For the smaller share of middle-class Americans who did this — primarily through retirement accounts like 401(k)s — it was overwhelmingly the best decision they made over the last fifty years. Most people didn’t do this in any serious way. But the people who did either kept up, or pulled ahead.

Now, imagine — and yes, this might already be happening to someone reading this — that your paycheck disappears. Suddenly, you’re leaning on the remaining three.

Two-earner households don’t help, because the second earner’s job is probably gone too. Debt requires income to service. And you can’t borrow your way through a period with no wages at the end of it. Home equity is real, but it’s not the kind of thing you can just take out without selling the house — and home prices need buyers with paychecks to support them.

That leaves the fourth one. Owning the assets.

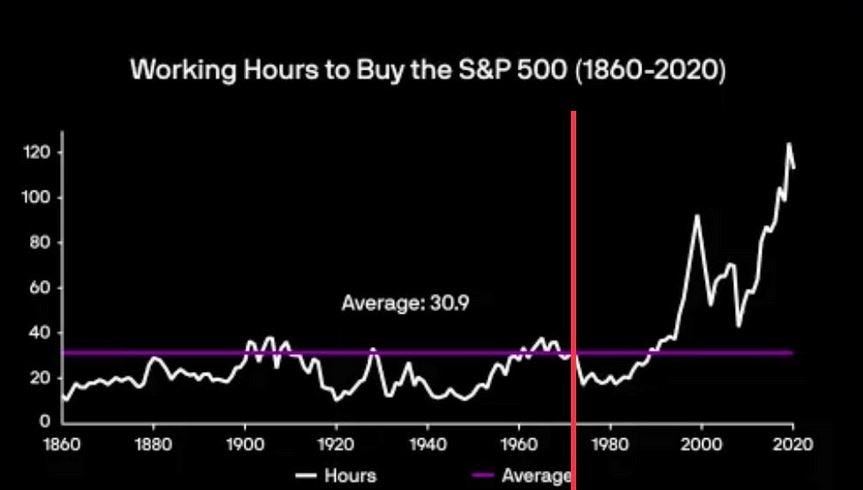

And look, if you want to see how badly the people who didn’t own assets got squeezed over the last fifty years, this chart tells the story. It shows how many hours of work it took to buy one unit of the S&P 500 since 1860.

Note: The S&P 500 itself only dates to 1957 (the S&P 90 started in 1926). The pre-1926 data is a standard back-extrapolation, built from Shiller's reconstructed series using individual stock data and earnings going back to the 19th century.

In other words, the productivity gains that didn’t go to wages went to the people who owned the assets. Here’s the breakdown of what happened to the major asset classes since 1971 (incl. the S&P 500):

Gold: $35 to about $4,400. Roughly 125x.

Silver: about $1.55 to roughly $73 today. Roughly 47x (with much bigger swings along the way).

S&P 500: 100 to about 7,400. Roughly 75x on price alone (much more with dividends reinvested).

Even if all you owned was your house, you did OK. The median American home went from about $25,000 in 1971 to roughly $419,000 today. That’s a 16x return.

Mind you, those are nominal numbers. The dollar lost most of its purchasing power over the same period, so the real returns are less impressive. But the point holds. Own the assets and you had a chance at staying ahead. Sell only your labor and you ran in place.

My guess is that what’s coming over the next twenty years is the same process, but compressed and worsened. The post-1971 generation lost real wages slowly. The post-2030 generation will lose wages entirely, and have them replaced with a state check whose buying power degrades on a fixed schedule.

The moral of the story? You’d better start learning about investing (and speculating). And practicing what you learn, too. Not necessarily to become rich, mind you — though many folks will. Just to keep your head above water in the world being assembled around you. Just to hold onto the kind of financial freedom your parents or grandparents probably took for granted.

Regards,

Lau Vegys

P.S. A quick note. I want to say thank you, sincerely, to everyone who has pledged your support over the past few weeks. I’m doing my best to reach out to each of you individually in private, but in case I missed anyone, thank you, again. I see the names. I read the messages. I do not take any of it for granted. Whether you’ve reached out publicly, privately, or just quietly clicked through to subscribe, I value it enormously. This essay — and the rest of what I’m trying to build — is possible because of you.

So well written and I think you’re really nailing a very complex problem - our current situation = I’m richer and wiser from this article - and many of your other wonderful articles.

The rise of the Ai-stockracy !