AI IPO Mania Is Here. You're the Exit Liquidity.

SpaceX at $1.75 trillion. OpenAI and Anthropic at roughly $1 trillion each. And your 401(k) is required to buy all three.

So three of the most powerful men in tech (one of them the richest person on earth) are about to sell you the most expensive shares in history. All of it this year, in 2026. And the thread that runs through all three is artificial intelligence, the same handful of companies whose names you haven’t been able to escape for the last twelve months.

Now, over the past week or two I’ve been writing a fair bit about AI. About its power to make you, in economic terms, go the way of the horse. And about how there’s really no avoiding owning these companies anymore, whether you want to or not. And honestly, I can’t think of anything that will shape your financial life more than this over the coming decades.

But I'd half-decided to give the subject a rest this week. Well, it turns out I can't. Because one of these sales (one of these IPOs, I should say) is happening this week. Three days from now, in fact. (And the other two are only months behind it.)

I’m talking about Elon Musk’s SpaceX, which goes public on June 12 in what may turn out to be the biggest IPO in human history (more on that below). Now, before you tell me SpaceX is a rocket company, let me stop you right there. It’s an AI company too, at least in part. You may not know this, but a few months ago Musk folded his AI company, xAI, into SpaceX at a $250 billion valuation.

Note: xAI makes Grok, which holds something like 3% of the AI market and burns through roughly a billion dollars a month. The merger also dragged in X, the social network formerly known as Twitter.

I’ll come back to all of that. But I want to be clear up front about what this essay actually is. Because the SpaceX IPO is going to eat the financial press for the next two weeks, and my bet is that most of the coverage will miss the point entirely. This isn’t really a story about SpaceX. It’s a story about a playbook: a way of moving money out of your pocket (your retirement account, to be specific) and into the hands of a small group of insiders. SpaceX is simply the one with a date on the calendar, and it happens to lay the whole thing out cleanly. So that’s where we’ll start.

Priced for Mars

OK, so the first thing to understand about the SpaceX IPO is the sheer size of it. Like I said, it may turn out to be the biggest in human history. (IPO just means initial public offering: the first time a private company sells its shares to the public.)

SpaceX priced its shares at $135 each. That values the whole company at about $1.75 trillion.

To see what kind of number that is, look at the company that held the “biggest IPO ever” title before it: Saudi Aramco. Aramco is the state oil company of Saudi Arabia, the outfit that pumps and sells a good slice of the crude the whole world runs on. When it went public in 2019, it listed at a valuation of around $1.7 trillion. So SpaceX is coming to market priced like the most valuable company ever floated.

There’s a catch, though. Aramco has always been wildly profitable. It sells oil, the one thing the entire planet still can’t run without. SpaceX lost roughly $6 billion last year.

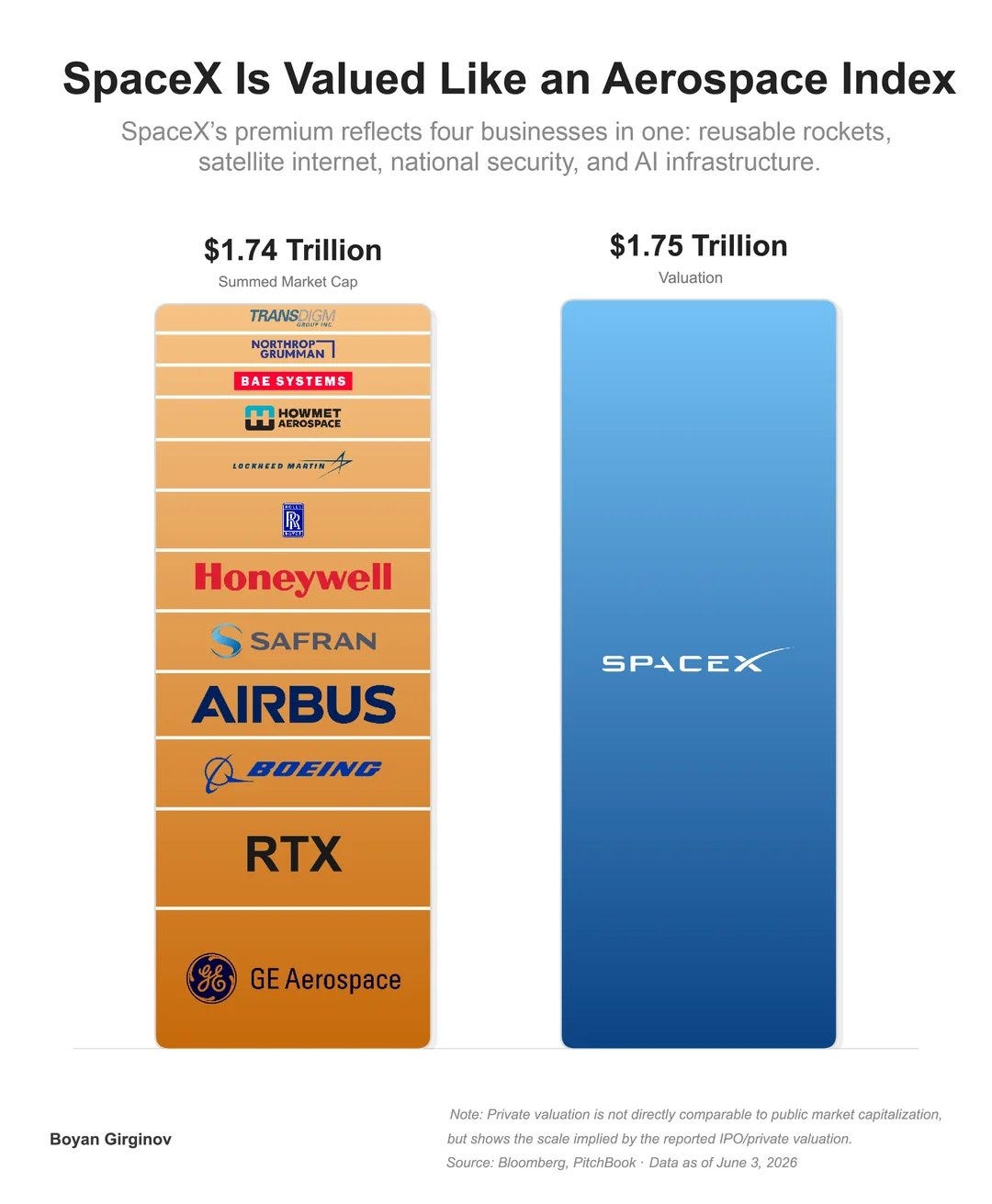

Either way, this is a giant. At $1.75 trillion, SpaceX would be one of the seven most valuable companies in America the moment it lists. On its own, it would be worth about as much as the dozen biggest aerospace and defense companies on the planet combined: Boeing, Airbus, RTX, Lockheed Martin, GE Aerospace, and the rest of the sector's giants stacked together.

The company is really three businesses. There’s Starlink, the satellite-internet arm, which is genuinely good: about $11 billion in revenue last year and $4.4 billion in operating profit. There’s the rocket business (the launches everyone pictures when they hear the name), which brought in around $4 billion, growing slowly, most of it flights SpaceX runs for its own satellites. And there’s the AI piece, xAI, the one I mentioned up top: roughly $3 billion in revenue and losing money by the billions.

Note: xAI was Musk’s own private company, and a few months ago he simply folded it into SpaceX at a $250 billion price tag. Because both companies were private, and Musk controls both, there was no outside market to argue with that number. He essentially set xAI’s $250 billion valuation himself.

Now do the back-of-the-envelope math the market is supposed to do. Put a rich multiple on Starlink, say fifteen times revenue, which is generous for almost any business, and you get around $170 billion. Be kind to the rockets and call that another $20 or $30 billion. As for the AI arm, it’s burning cash hand over fist and hard to value at all. But let’s be generous, give Musk the benefit of the doubt, and use his own $250 billion figure for it.

Add all of that up with a very generous hand, and the parts of SpaceX that actually exist and sell something come to maybe $450 billion. That isn’t even in the same postcode as the asking price.

So what fills the gap, the trillion-plus in between? Nothing that resembles revenue. It’s the story. Mars. Orbital data centers. The light of human consciousness reaching the stars.

Great stuff. But strip all of that out, and what you’re left with is a company being sold at about ninety times its annual sales. For context, Facebook went public at roughly eleven times sales, and people thought that was rich. Google listed at five or six.

You don’t have to take my back-of-the-napkin math for it, either. Morningstar (the investment-research firm that puts price tags on companies for a living) values SpaceX at about $780 billion. That’s quite a bit more generous than my number. And it’s still less than half the asking price.

So with those figures in front of you, the question almost asks itself: who actually pays $1.75 trillion for a company that, by every visible measure, looks worth a fraction of that?

The Only Buyer Big Enough

Well, to pull something like this off, you don’t just need buyers. You need a lot of them. And, more importantly, you need the kind of buyers who’ll show up and buy no matter what the company is actually worth.

There’s exactly one pool of money on earth that fits that description. It’s the passive money: the 401(k)s and index funds sitting in nearly every retirement account in America.

Here’s how that works.

As you’re probably aware, most people don’t pick their own stocks. Their retirement savings sit in index funds, funds that don’t research anything and don’t judge whether a stock is cheap or dear. They make exactly one promise: to mirror a list. The S&P 500. The Nasdaq-100. Whatever is on the list, in whatever proportion, the fund holds it, so your money simply tracks “the market.” That’s the whole product, and it’s gigantic. Trillions of dollars, the default setting in most 401(k) plans in the country. Probably yours included.

Now, a fund like that doesn’t look at SpaceX’s $6 billion loss and decide to take a pass. It can’t. The moment SpaceX is added to the index, every fund tracking that index has to go out and buy it, at the same time, in the same proportion, at whatever price the market happens to be asking that week. There’s nobody weighing whether it’s a good deal.

And that is very good news if you happen to be an insider. By insiders I mean the people who already own most of SpaceX (the early investors, the venture funds, the executives, Musk himself), the ones who bought in years ago at a tiny fraction of today’s price. On paper, they’re sitting on enormous fortunes. But paper isn’t money. To turn it into money, they have to sell. And to sell billions of dollars of stock without crashing the price, they need a wall of buyers waiting on the other side.

That’s exactly what the index hands them. The insiders cash out at the top. You’re left holding the stock. Congratulations. You’ve just been used as exit liquidity.

Now, maybe you’re thinking it’s not that bad. Musk is a visionary (nobody can really argue with that), and maybe SpaceX does go on to colonize Mars, blanket the planet in Starlink, and run the data centers of the future from orbit. Sure, that might all happen. I don’t know that it won’t.

What I do know is this. A man named Jay Ritter, a University of Florida professor who has tracked thousands of IPOs for decades, has shown the same thing over and over: newly public companies tend to lag the market in the years after they list, and the richer the price at the offering, the worse they tend to do. And remember, SpaceX is coming at ninety times sales.

There’s another piece of context worth holding onto here, and it comes from Musk’s own back catalogue: Tesla, the electric-car company he’s still best known for. In December 2020, Tesla was added to the S&P 500, at the time the largest company ever brought into the index, and only after a run-up of more than 70% on the announcement. Every index fund in America was forced to buy it at that peak. Three years later, Tesla was up about 6%. The S&P 500 over the same stretch was up around 27%. The passive investors marched in at the top spent three years underperforming the very index they were part of, while the early holders took their gains and walked.

Then again, Tesla did work out in the end, so maybe this one will too.

SpaceX Is Just the First

But remember, as I mentioned in the intro, SpaceX is only one of three giant IPOs lined up this year. It’s the biggest, and the first to arrive, but really it’s just the door swinging open. Right behind it come the other two. OpenAI, the maker of ChatGPT, filed on June 8 and is expected to follow this fall at more than $1 trillion. And Anthropic, the maker of Claude, filed on June 1 at around $960 billion.

That’s quite a lineup. Three of the most hyped companies on earth, all elbowing toward the same exit at once, all trying to sell their shares to you inside the same few months. Which begs the obvious question: why? Why the stampede?

The short answer is that the window is closing, and the people on the inside can see it more clearly than anyone.

The longer answer is a combination of a few things. Let me walk through them.

The first reason is the simplest: they need the money, and they’re running out of places to get it. AI devours cash on a scale that’s hard to fathom. The four biggest tech companies alone are pouring some $725 billion into it this year. That’s up nearly 80% from last. The companies now lining up to go public have their own enormous bills, and for years private investors footed them, round after round. That private money is drying up. The public market is the biggest pool left, so when you need to raise tens of billions, that’s where you go.

The second is timing. The boom holds only as long as everyone believes the valuations, and an IPO is where that belief first meets daylight. In a market this stretched, one flop can turn the mood and slam the window shut, leaving whoever’s last in line to list into a colder market for a fraction of the price, if at all. So nobody wants to be last. It doesn’t even have to be SpaceX that breaks the spell; any over-hyped debut will do. Better to go early and be clear before someone else’s bad listing ends the party.

Fair enough. But are these companies even making money?

Well, OpenAI is on track to lose around $14 billion this year, with no profit expected until 2030. It has signed up for roughly $1.4 trillion in future computing bills against maybe $25 billion of revenue. Remember, it wants to go public at ~$1 trillion. That’s the SpaceX problem all over again, only without a Starlink underneath to cushion it.

Anthropic, to be fair, is the exception: it’s actually closing in on its first profitable quarter (its first, mind you, not a track record of them), and at around twenty times sales it’s the only one of the three you could call sensibly priced. But that’s almost beside the point. Because whether these companies are any good or not, the index doesn’t care. Profitable or bleeding, your retirement funds will be forced to buy them.

In Closing…

This essay is already long, so I’ve skipped over a few things, like the fact that SpaceX didn’t even qualify for fast index inclusion under the old rules, and that Nasdaq quietly rewrote them so it could be force-fed into the index anyway, reportedly at Musk’s own insistence.

But the mechanics aren’t really the point. The point is that this is a playbook, and it won’t expire when the SpaceX window closes. Everything I’ve seen looking into this tells me that the nature of the AI business (staggeringly expensive, deeply unprofitable, and utterly dependent on a constant supply of fresh money) means its founders will keep needing to turn you into an unwilling, and largely unwitting, shareholder in their companies. That’s just the truth of it.

Now, once again, you don’t get a vote on what the index buys. So this week, and then again in the fall, and again later this year, your index funds are going to own SpaceX, then OpenAI, then Anthropic, at whatever price the market sets that week. Nobody is going to call and ask your permission.

The least you can do is not be surprised by it.

And if you’re really clear-eyed about it, you can go one step further: own a few things that don’t depend on an index committee, a Fed chair, or an IPO clearing at a price somebody’s praying it clears at. It may sound cliché, but if you ever needed one more reason to own unprintable assets like gold and silver, this is it.

Regards,

Lau Vegys

P.S. A quick note. I want to say thank you, sincerely, to everyone who has pledged your support over the past few weeks. I’m doing my best to reach out to each of you individually in private, but in case I missed anyone, thank you, again. I see the names. I read the messages. I do not take any of it for granted. Whether you’ve reached out publicly, privately, or just quietly clicked through to subscribe, I value it enormously.

Phenomenal article- this is the type of stuff the Main Street media is SUPPOSED to report. Thank you for what you do. I never miss a Lau Article

If your company allows it, going self-directed on your 401(k) is the only way to avoid this garbage.